Internal vs external financial reporting explains how companies use two separate accounting systems: one for managing daily decisions and control, and another for reporting performance to outside stakeholders under strict rules.

At first glance, accounting looks like a single system that produces reports at the end of the month or year. But in real businesses, accounting serves two different audiences at the same time. Managers inside the company need detailed, fast-moving information to run operations, while investors, lenders, and tax authorities need standardized, verified reports.

This split is not accidental—it is built into how modern accounting systems work. Once you understand this separation, financial reports become easier to read and much more useful in real decision-making.

One key idea appears repeatedly across financial systems: the same raw data can serve completely different purposes depending on who is using it and why.

Takeaways

- Internal reporting focuses on running and controlling daily business operations.

- External reporting focuses on compliance, transparency, and stakeholder communication.

- The same accounting data can be reshaped into different reports depending on the audience.

- GAAP-based reporting standardizes financial information for investors, lenders, and regulators.

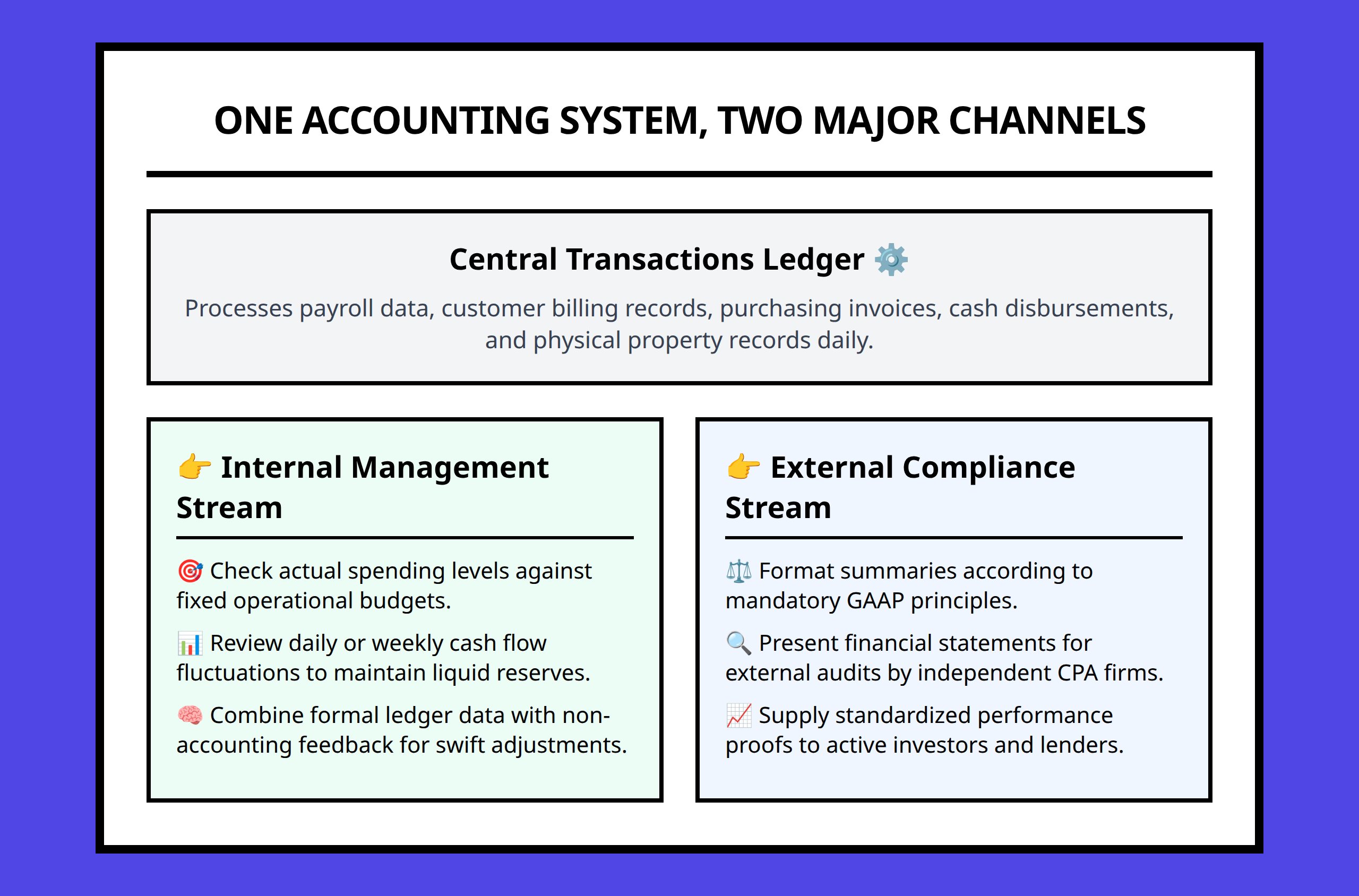

The Accounting System’s Dual Purpose

Accounting systems are designed to serve two different purposes at the same time: internal decision-making and external reporting. These two functions share the same financial data but transform it differently depending on the goal.

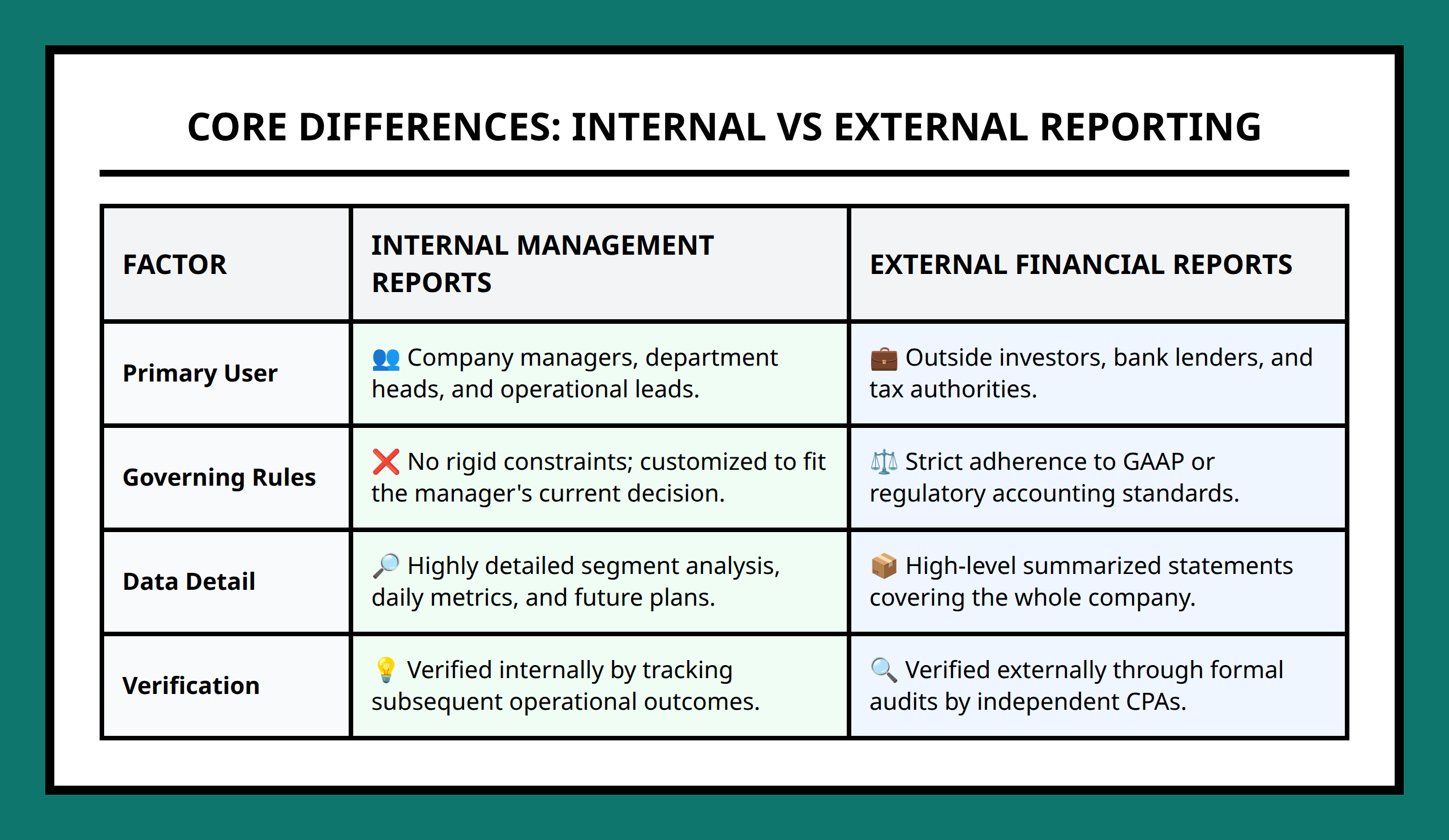

Internal reporting is used by managers to run the business. It includes detailed operational data such as payroll costs, billing activity, purchasing trends, cash disbursements, and property records. These reports are not heavily standardized because they are meant for internal use only.

For example, a warehouse manager may receive a weekly report showing $48,000 in shipping costs broken down by supplier and route. That same level of detail would not appear in external financial statements, but it is essential for operational control.

External reporting, on the other hand, is designed for people outside the business. This includes investors, lenders, auditors, and tax authorities. These reports must follow strict accounting standards to ensure consistency and fairness across companies.

External reports summarize performance rather than explaining operational details. They answer questions like: Did the company make a profit? How much cash did it generate? What is its financial position at the end of the period?

Because these two purposes are so different, businesses maintain structured financial reporting systems that separate internal detail from external summaries.

Management Control and Decision-Making Reports

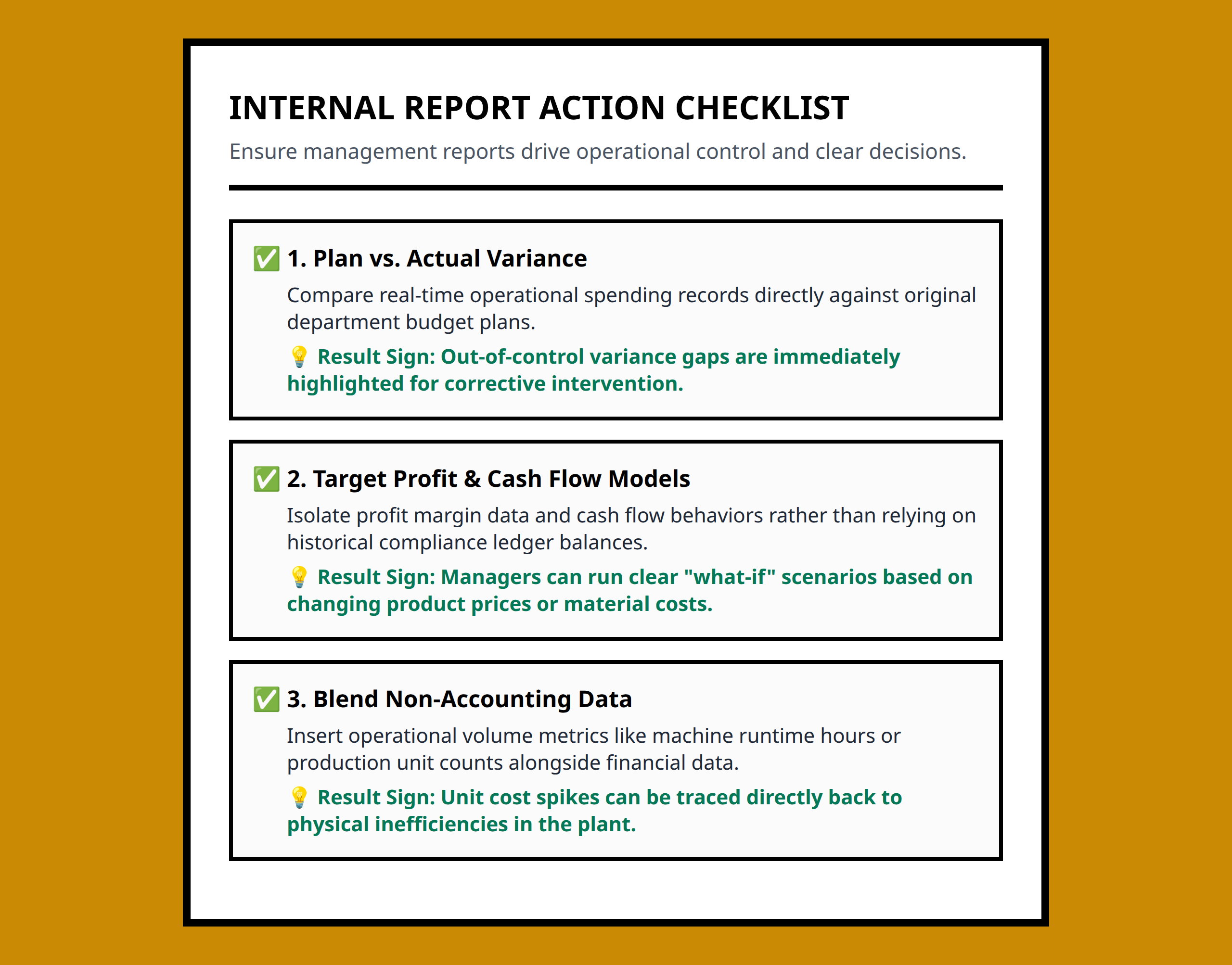

Management control reports are one of the most important tools in internal accounting. Their purpose is to compare actual performance against planned or expected performance.

For example, a company may set a monthly sales target of $500,000 for a regional team. A control report would show actual sales performance side-by-side with this target, highlighting gaps such as underperformance in a specific product line or region.

These reports are not just about numbers—they are about action. When a deviation appears, managers can respond quickly by adjusting pricing, reallocating staff, or changing purchasing plans.

Decision-making reports go a step further. Instead of focusing only on comparisons, they help managers evaluate future choices using financial data. These reports often focus on profit forecasts and cash flow models.

For instance, a business considering a new product launch might review projected cash flow under different pricing scenarios. One scenario might show a $120,000 monthly inflow, while another shows slower but more stable growth. These insights help leaders choose the most sustainable path.

Importantly, not all inputs in these reports come from accounting data alone. Non-accounting information—such as customer demand, production capacity, or supplier reliability—often plays a critical role in shaping decisions. This combination makes internal reporting more flexible and more detailed than external reporting.

External Reporting and Regulatory Requirements

External financial reporting follows strict rules to ensure accuracy, consistency, and transparency. The most widely used framework is Generally Accepted Accounting Principles (GAAP), which defines how financial statements must be prepared.

GAAP ensures that companies report financial results in a consistent way, making it easier for investors and lenders to compare performance across businesses. Without these standards, financial statements would vary too much to be useful for external decision-making.

External reporting includes three core financial statements: the income statement, balance sheet, and cash flow statement. These reports are reviewed by auditors, often from certified public accounting (CPA) firms, to ensure accuracy and compliance with regulations.

For example, an audited income statement may show total revenue, expenses, and net income for the year, but it will not include detailed breakdowns like internal payroll or supplier-level purchasing data. The goal is clarity, not operational detail.

External reporting also includes tax reporting obligations. Businesses must prepare tax returns covering income taxes, payroll taxes, property taxes, and sales taxes. These reports are required by law and must align with financial records to ensure compliance.

Unlike internal reports, external reports are not designed to help managers adjust daily operations. Instead, they are designed to meet legal requirements and provide transparency to external stakeholders such as investors, banks, and regulators.

How Internal and External Reporting Work Together

Even though internal and external reporting serve different purposes, they are built on the same financial foundation. Every transaction recorded in the accounting system can flow into both types of reports.

For example, when a company processes payroll, the internal system may break down wages by department, job role, and overtime hours. At the same time, the external system aggregates that data into total labor expense for financial reporting purposes.

Similarly, purchasing systems may track individual supplier invoices internally, while external reports only show total cost of goods sold or operating expenses.

This shared foundation ensures consistency while still allowing flexibility in how information is presented. It also reduces duplication of effort, since the same underlying data supports multiple reporting needs.

However, the interpretation of that data changes depending on the audience. Internal users focus on detail and control, while external users focus on summarized performance and compliance.

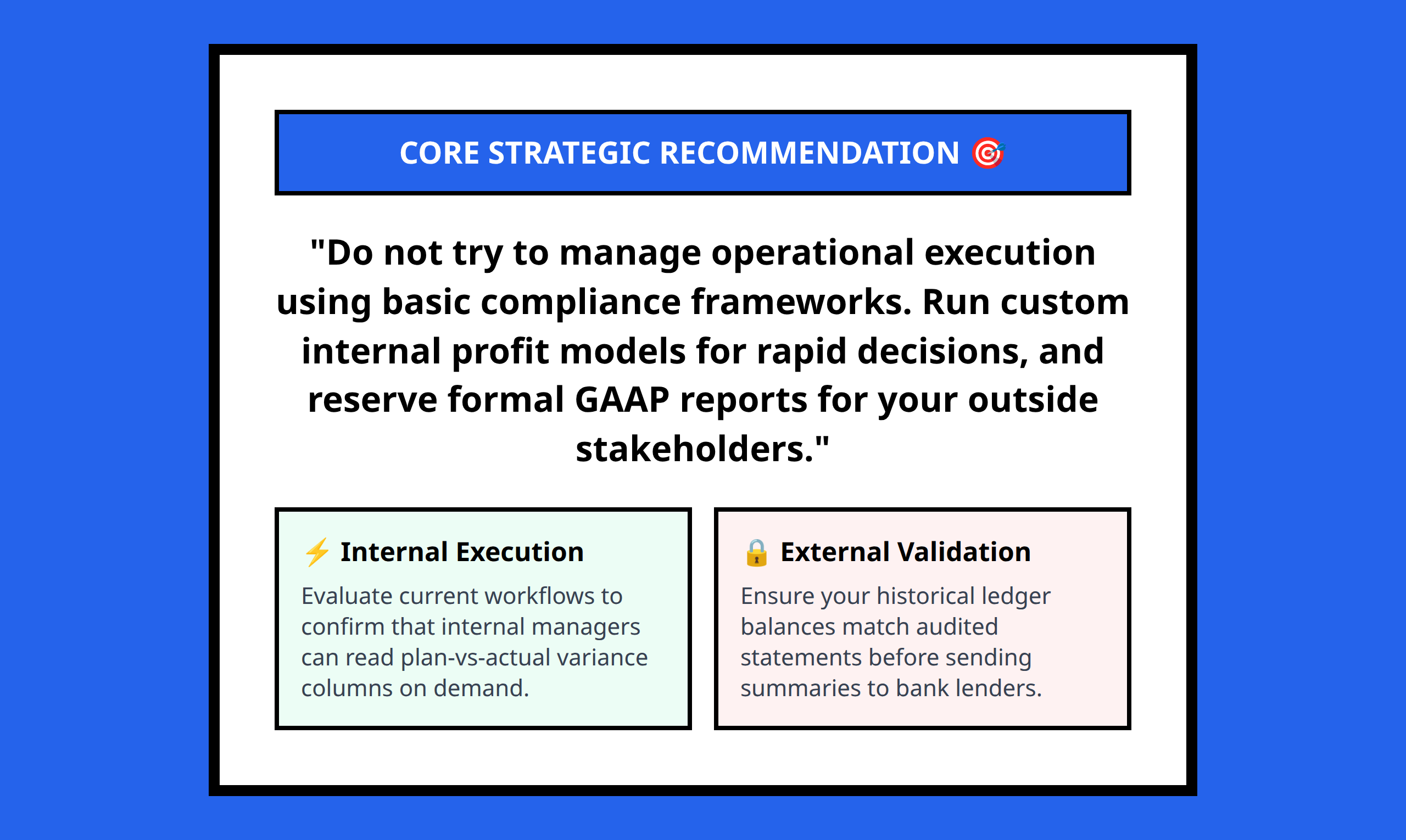

Why This Distinction Matters in Real Business Decisions

Understanding the difference between internal and external reporting is essential for avoiding common financial misunderstandings.

For example, a company might appear highly profitable in external reports, but internal reports could reveal rising production costs or declining efficiency in a specific department. Without internal detail, management might miss early warning signs.

On the other hand, internal reports might show strong operational efficiency, but external reports could highlight concerns about overall profitability or cash flow stability. Both perspectives are necessary for a complete financial picture.

This is why businesses rely on both systems simultaneously. One ensures compliance and external trust, while the other ensures operational effectiveness and internal control.

FAQ

Key Terms Explained

- Internal Financial Reporting: Accounting reports used by managers to control operations, analyze performance, and make business decisions.

- External Financial Reporting: Standardized financial statements prepared for investors, lenders, regulators, and tax authorities.

- GAAP: Generally Accepted Accounting Principles that define how financial statements must be prepared and presented.

- Management Accounting: The process of using financial data for internal planning, control, and decision-making.

- Financial Statements: Structured reports such as the income statement, balance sheet, and cash flow statement that summarize business performance.

When reviewing any financial report, the most useful question is simple: is this designed to help manage the business internally, or is it designed to communicate results externally? The answer changes how you should interpret every number on the page.

References:

- https://corporatefinanceinstitute.com/resources/accounting/internal-vs-external-financial-reporting/

- https://www.wallstreetoasis.com/resources/skills/accounting/internal-vs-external-financial-reporting

- https://www.netsuite.com/portal/resource/articles/accounting/financial-reporting.shtml

- https://linfordco.com/blog/internal-vs-external-audits-explained/

- https://www.jrcpa.com/financial-reporting-and-the-4-levels-of-service/

- https://quizlet.com/au/108590290/internal-and-external-reporting-flash-cards/

- https://www.inscopehq.com/post/internal-vs-external-audit-key-differences-and-benefits

- https://www.diligent.com/resources/blog/three-keys-to-effective-internal-control-over-financial-reporting

- https://www.heflo.com/blog/internal-controls-vs-external-controls