Profit reflects accounting performance within a time period, while cash flow reflects actual liquidity movement—and the two often differ due to timing gaps in transactions. Understanding this difference is essential for making sound financial decisions.

One of the most confusing moments for anyone learning business finance is realizing that profit does not equal cash. At first glance, it feels like a contradiction. If a business shows a profit, shouldn’t it also have the cash to match?

The reality is more subtle. Profit and cash flow are built from different rules. One follows when economic activity happens, and the other follows when money actually moves. Once you see this clearly, financial statements become much easier to interpret—and much more useful in real decisions.

Takeaways

- Profit and cash flow measure two different realities: performance vs liquidity.

- Timing differences in receivables and payables create most gaps between the two.

- A business can be profitable but still face cash pressure in the same period.

- Understanding both views is necessary to avoid misleading financial conclusions.

The Core Reason Profit and Cash Flow Differ

The main reason profit and cash flow do not match is timing. Profit follows accrual rules, which record revenue when it is earned and expenses when they are incurred. Cash flow, on the other hand, records actual money received or paid.

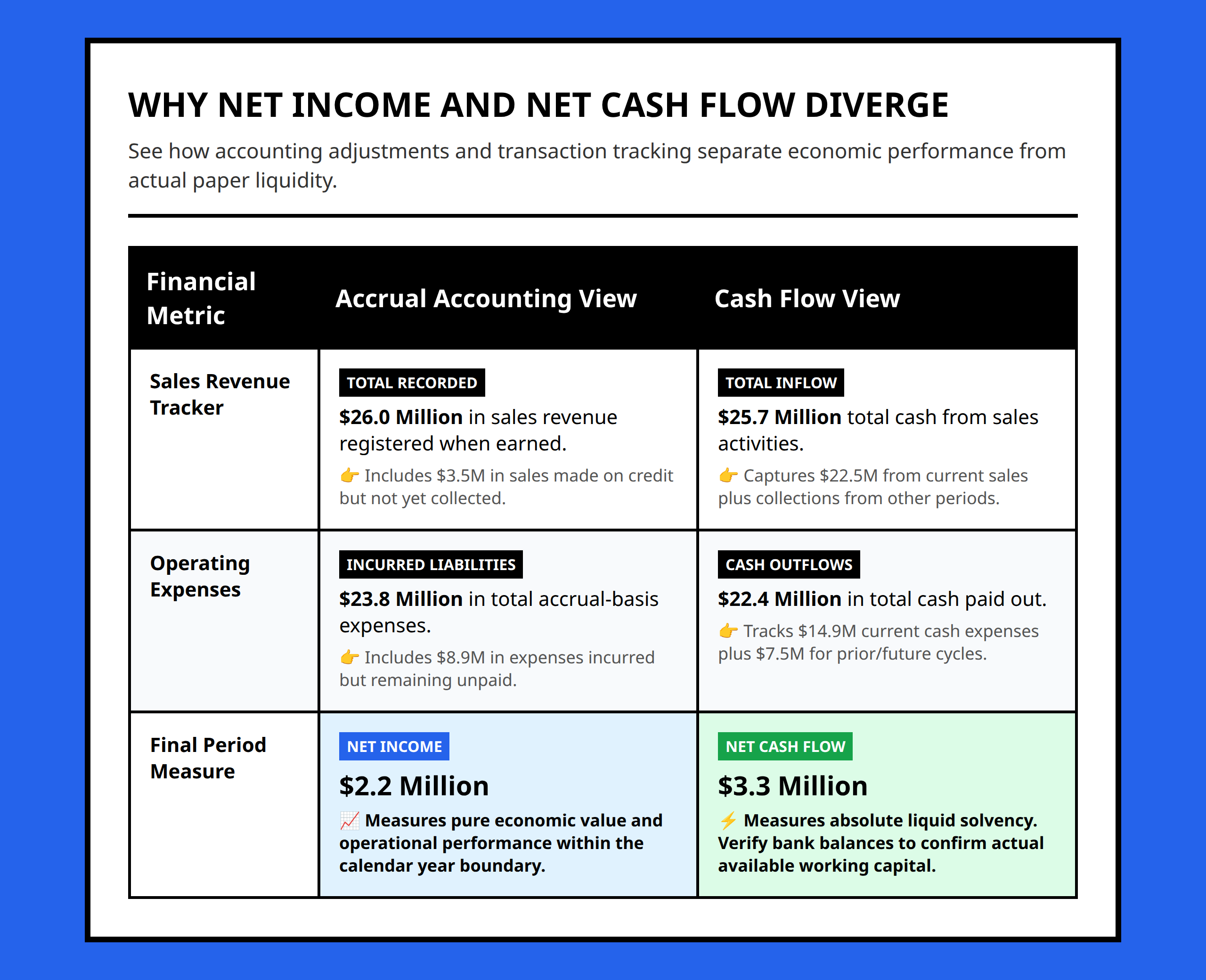

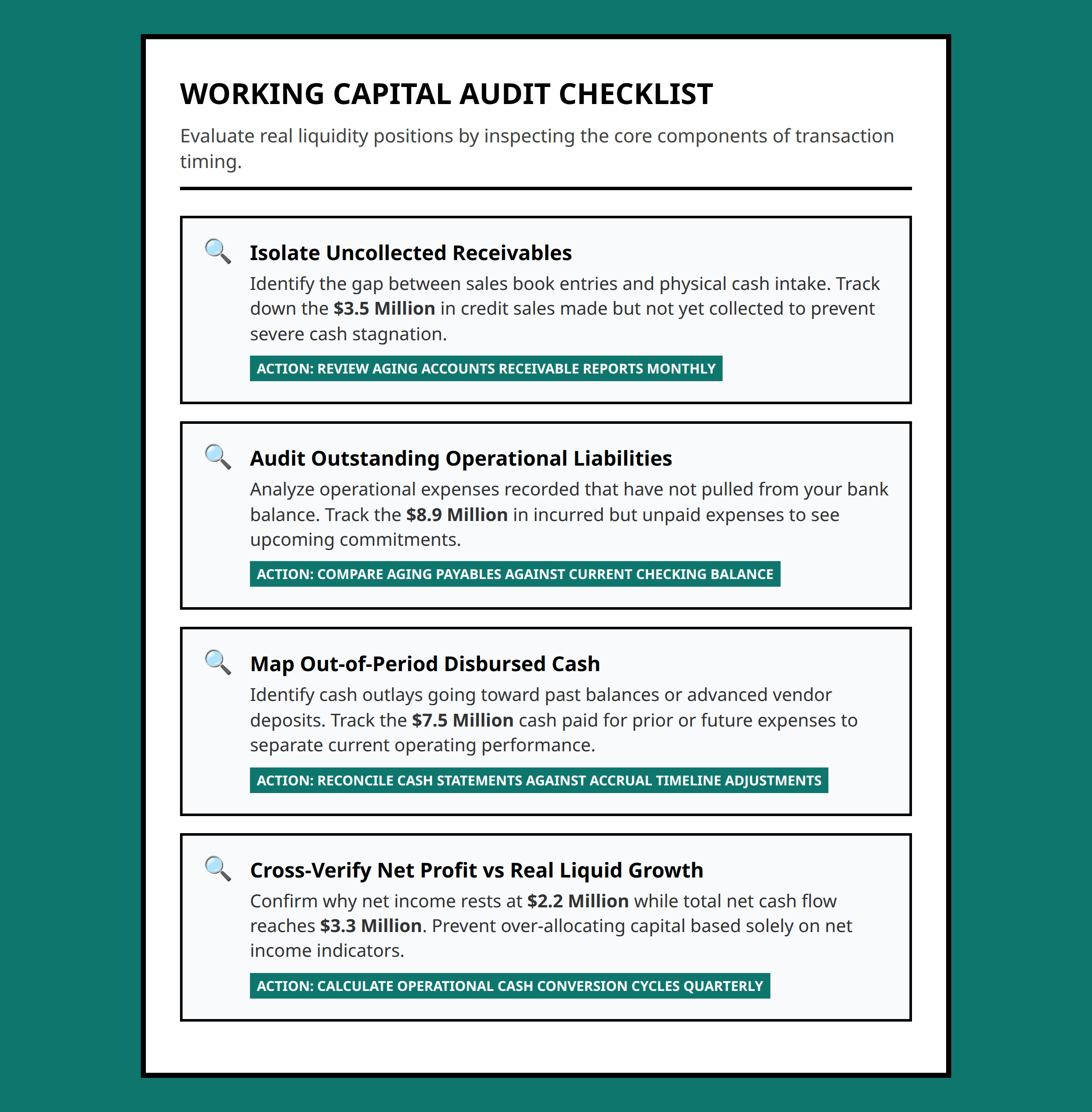

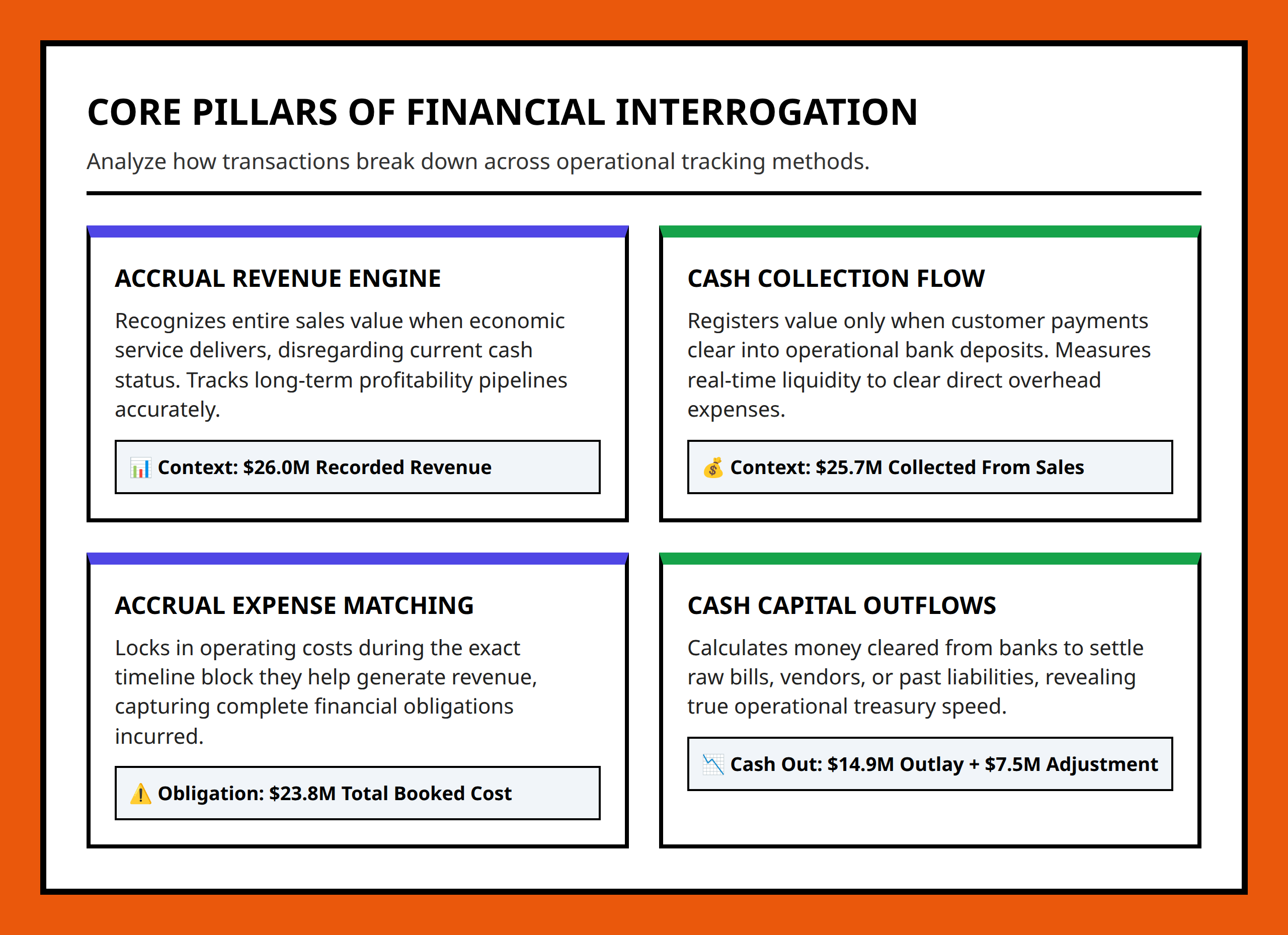

This creates a natural gap between financial performance and liquidity. For example, a business may report $26.0 million in sales revenue for the year, but only $22.5 million is collected in cash from those same sales during the period. The remaining $3.5 million represents sales made but not yet collected.

That difference alone shows how profit can exist without immediate cash inflow. Revenue is recognized based on delivery and earning, not payment.

Expenses follow a similar pattern. A company may record $23.8 million in total expenses for the year, but only $14.9 million is actually paid in cash during the same period. The remaining $8.9 million represents expenses incurred but not yet paid.

This timing mismatch explains why profit does not reflect cash movement directly. It is not an error—it is the structure of accrual accounting.

Breaking Down a Real Business Cash Flow Structure

To understand the gap more clearly, it helps to separate the cash and accrual components of business activity. A business can appear financially strong under profit measurement while its cash movements tell a more complex story.

In a typical operating cycle, cash comes in from multiple directions. For example, during a single year, a business might collect $22.5 million in cash from current-year sales. At the same time, it might also collect $3.2 million from previous or future sales transactions, bringing total cash inflow related to sales to $25.7 million.

On the expense side, the cash story is equally layered. The business may pay $14.9 million in cash for expenses recorded in the current year, while also paying $7.5 million for expenses related to earlier or later periods. This creates a total cash outflow for expenses of $22.4 million.

What matters here is not just the totals, but how timing reshapes them. Cash does not follow the same boundaries as accounting periods. It flows across them.

This is why working capital timing differences are so important. Receivables and payables act like buffers between performance and liquidity. When they grow, cash becomes tight even if profit looks healthy. When they shrink, cash improves even if profit does not change much.

Why Net Income and Net Cash Flow Diverge

Once timing differences are combined, the separation between profit and cash flow becomes clear. Net income is calculated using accrual-based rules, while net cash flow reflects actual inflows and outflows during the period.

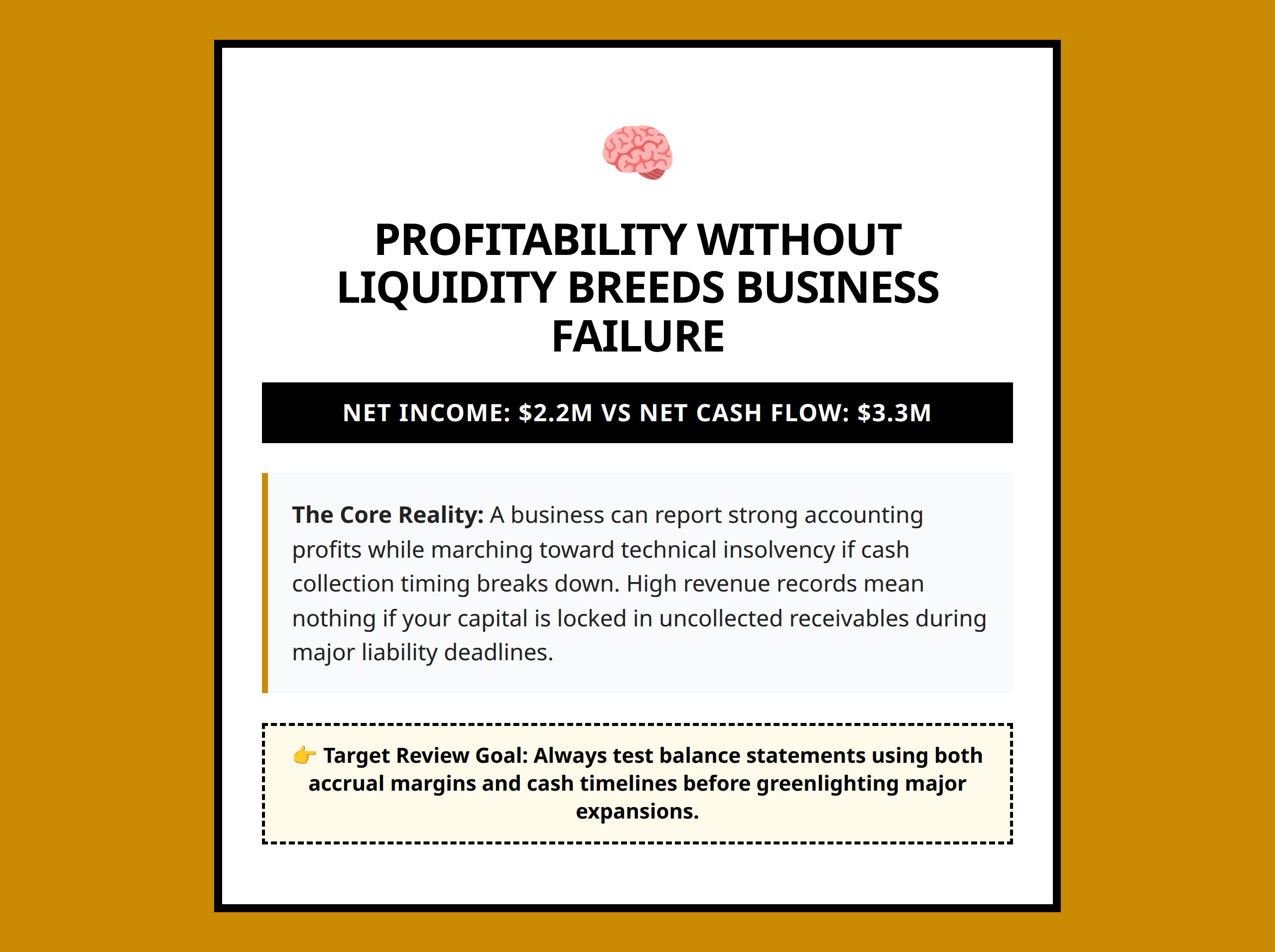

In this case, the business reports a net income of $2.2 million. This is the result of subtracting $23.8 million in expenses from $26.0 million in revenue.

However, the cash perspective tells a different story. The same business shows a net cash flow of $3.3 million for the year. This difference does not mean one figure is wrong. It means each figure is measuring something different.

The $2.2 million profit reflects economic activity that happened during the year. The $3.3 million cash flow reflects actual liquidity movement, including adjustments from timing differences in receivables and payables.

This is why businesses often experience situations where they are profitable on paper but still feel cash pressure—or the opposite, where cash looks strong even when profit is modest.

Another important detail is that total cash flow tied to operating activity is broader than just current-year transactions. When combining inflows and outflows, total cash movement from sales-related activity can reach $25.7 million in inflows and $22.4 million in outflows, reinforcing how dynamic cash movement is compared to static profit measurement.

Why Timing Differences Matter in Real Decisions

Understanding accrual accounting vs cash flow is not just theoretical. It affects real business decisions every day.

For example, a business might see strong profit numbers and decide to expand operations. But if most of its revenue is tied up in unpaid receivables—like the $3.5 million in sales not yet collected—it may struggle to fund that expansion.

Similarly, if a business has large unpaid expenses, such as the $8.9 million recorded but not yet paid, it may face sudden cash demands even if profit remains stable.

This is why financial analysis requires both perspectives. Profit shows whether the business model works. Cash flow shows whether the business can survive day-to-day operations.

In practice, managers often need to track both side by side. A business can tolerate temporary profit fluctuations, but it cannot survive prolonged cash shortages.

How to Read Profit and Cash Flow Together

The key to better financial interpretation is not choosing between profit and cash flow—it is combining them.

When profit is higher than cash flow, it often signals growth in receivables or delayed payments. When cash flow is higher than profit, it may indicate collection of earlier receivables or delayed expense recognition.

In the example structure we explored, the difference between $2.2 million profit and $3.3 million cash flow shows how timing can shift financial perception even when underlying operations remain stable.

Once this logic becomes familiar, financial statements become less abstract and more like a map of timing relationships rather than static numbers.

FAQ

- Accrual Accounting: A method of recording revenue when earned and expenses when incurred, regardless of when cash is exchanged.

- Cash Flow: The actual movement of money into and out of a business during a specific period.

- Revenue Recognition: The rule that determines when sales are recorded in financial statements.

- Receivables: Money owed to a business for goods or services already delivered.

- Payables: Money a business owes to suppliers or service providers.

When reviewing a business, the most useful question is not “Did it make a profit?” but “Where is the cash sitting right now—and why?” That shift in focus often reveals more about financial health than profit alone ever can.

References:

- https://www.investopedia.com/ask/answers/09/accrual-accounting.asp

- https://quickbooks.intuit.com/accounting/cash-vs-accrual-accounting-whats-best-small-business/

- https://www.netsuite.com/portal/resource/articles/financial-management/cash-basis-accrual-basis.shtml

- https://mercury.com/blog/cash-basis-vs-accrual-accounting

- https://www.youtube.com/watch?v=kINTtyXPGwM

- https://www.youtube.com/watch?v=CRcHPo-gP1M

- https://www.youtube.com/watch?v=j6tKOuKxq-8

- https://preferredcfo.com/insights/purpose-accrual-accounting

- https://www.wilsoncpallc.com/resources/blog/accrual-accounting-vs-cash-basis-accounting-whats-the-difference

- https://ramp.com/blog/cash-vs-accrual-accounting

- https://www.anchin.com/articles/cash-vs-accrual-accounting-key-differences-and-how-to-choose-the-right-method/