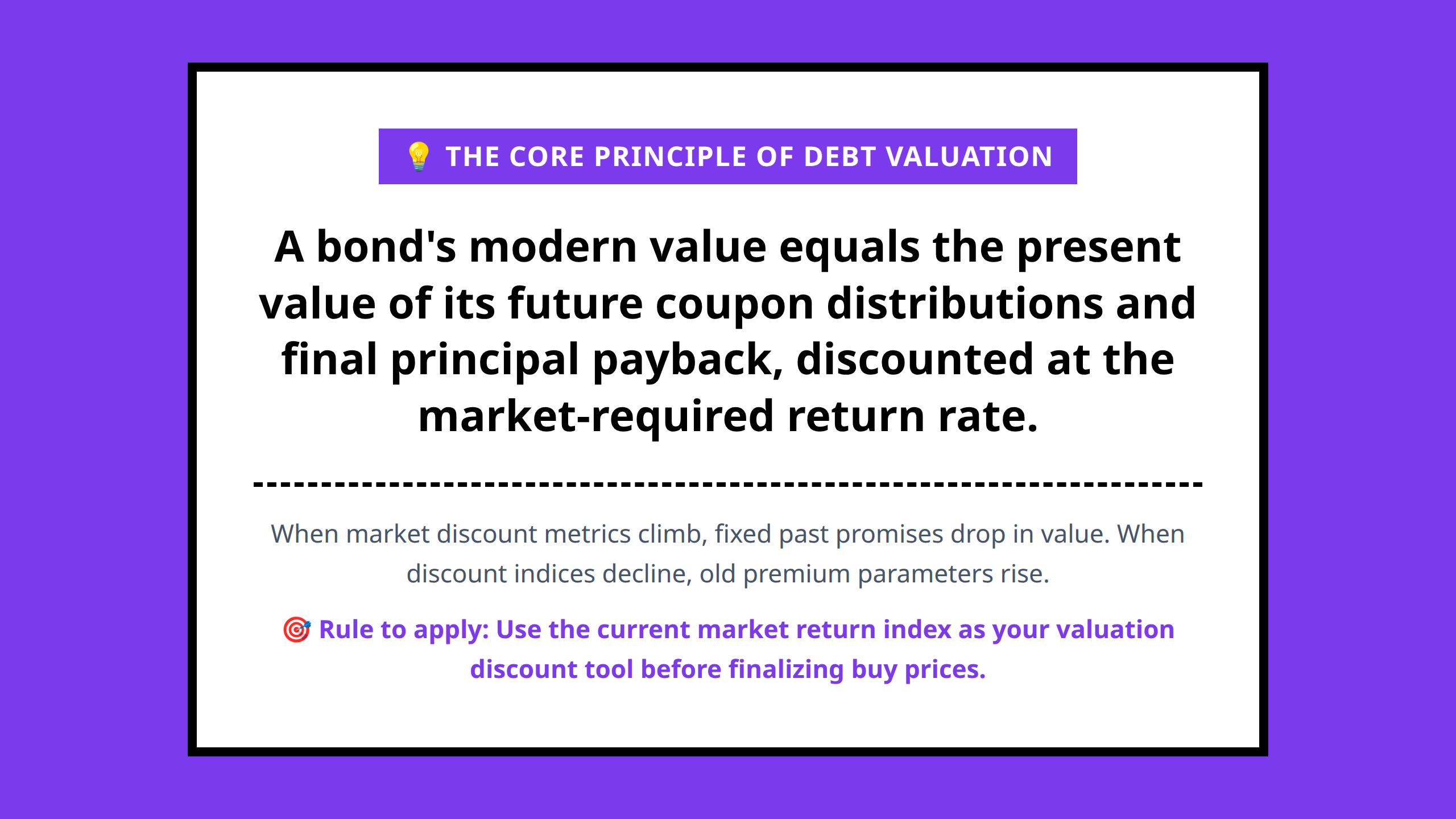

Bond valuation explains how a bond’s price is determined by the present value of its future coupon payments and final repayment, discounted using the market-required return. This framework also explains why bond prices fall when interest rates rise, and rise when interest rates fall.

Bond prices often confuse even people who are comfortable with basic investing. A bond may pay a fixed coupon, yet its market price constantly changes. This creates an illusion that bond value is unpredictable, when in reality the logic behind it is very structured and consistent.

Once you understand how future cash flows are discounted, bond pricing becomes much clearer. The key idea is simple but powerful: the value of money in the future depends on the interest rate environment today. This single principle explains most bond price movements in financial markets.

In this article, I want to break down bond valuation in a way that connects intuition with calculation. Instead of memorizing formulas, you will see how bond pricing naturally follows from discounting future payments back to the present.

Takeaways

- Bond prices are determined by the present value of future coupon payments and principal repayment.

- Interest rates and bond prices move in opposite directions due to discounting.

- The coupon rate is not the same as investor return; yield depends on market conditions.

- Longer maturity bonds are more sensitive to interest rate changes.

- Inflation and required returns play a major role in bond valuation.

The Building Blocks of Bond Valuation

To understand bond valuation, it is important to first understand what a bond actually represents. A bond is a contract where an investor lends money to an issuer in exchange for periodic interest payments and the return of principal at maturity.

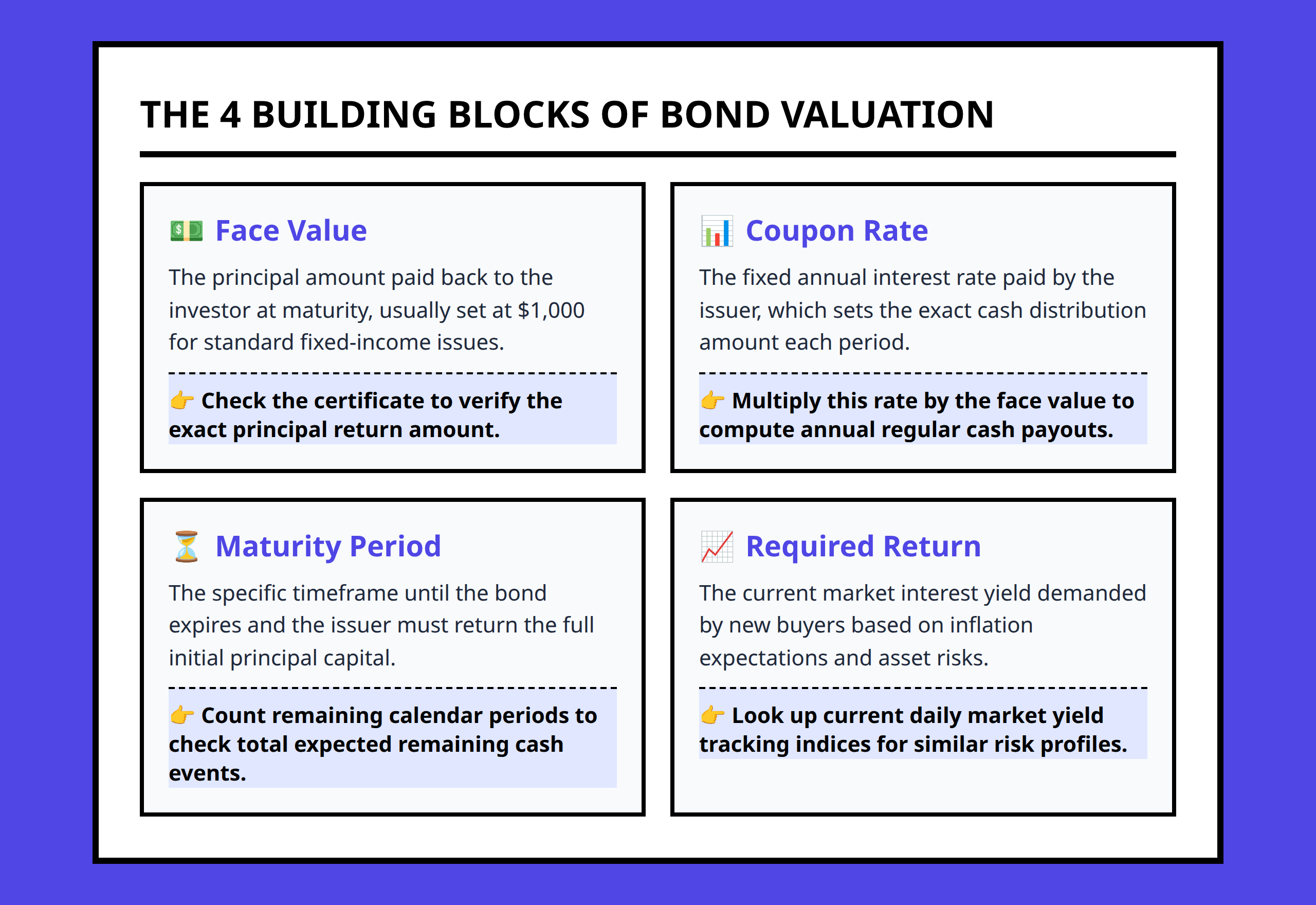

Every bond valuation process is built on four core components: face value, coupon rate, maturity, and required return. Each of these plays a specific role in determining the bond’s price in the market.

Face value: the anchor of repayment

The face value (or par value) is the amount the bond issuer agrees to repay at maturity. This is typically a fixed amount and serves as the baseline for the bond’s final cash flow.

Even though market prices may fluctuate above or below this value, the face value remains the amount returned at maturity under normal conditions.

Coupon rate: the periodic income stream

The coupon rate determines how much interest the bond pays each year. This is usually expressed as a percentage of the face value.

For example, a bond with a fixed coupon provides regular income to investors, making bonds attractive to those seeking predictable cash flows. However, the coupon rate alone does not determine total return.

Maturity: the time dimension of risk

Maturity refers to how long the bond will exist before the principal is repaid. This time horizon matters because longer-term bonds are exposed to more uncertainty and greater sensitivity to interest rate changes.

In general, the longer the maturity, the more the bond’s price reacts to changes in market interest rates.

Required return: the market’s discount rate

The required return is the rate investors demand for holding the bond. It reflects market interest rates, inflation expectations, and perceived risk.

This is the most important driver of bond pricing because it is used to discount future cash flows into today’s value.

Once these four elements are combined, bond valuation becomes a matter of calculating present value.

How Bond Prices Are Determined Using Discounted Cash Flows

The central principle of bond valuation is that a bond’s price equals the present value of all expected future cash flows. These include periodic coupon payments and the final repayment of face value.

Each future payment is discounted back to today using the required return. The farther in the future the payment, the lower its present value.

This is why bonds with longer maturities tend to have more sensitive pricing behavior. Their cash flows are exposed to discounting over a longer time horizon.

When market interest rates rise, the discount rate increases. As a result, the present value of future bond payments falls, reducing the bond’s price. When rates fall, the opposite happens: future payments become more valuable in today’s terms, increasing bond prices.

This mechanism explains the inverse relationship between bond prices and interest rates.

Why Interest Rates and Bond Prices Move in Opposite Directions

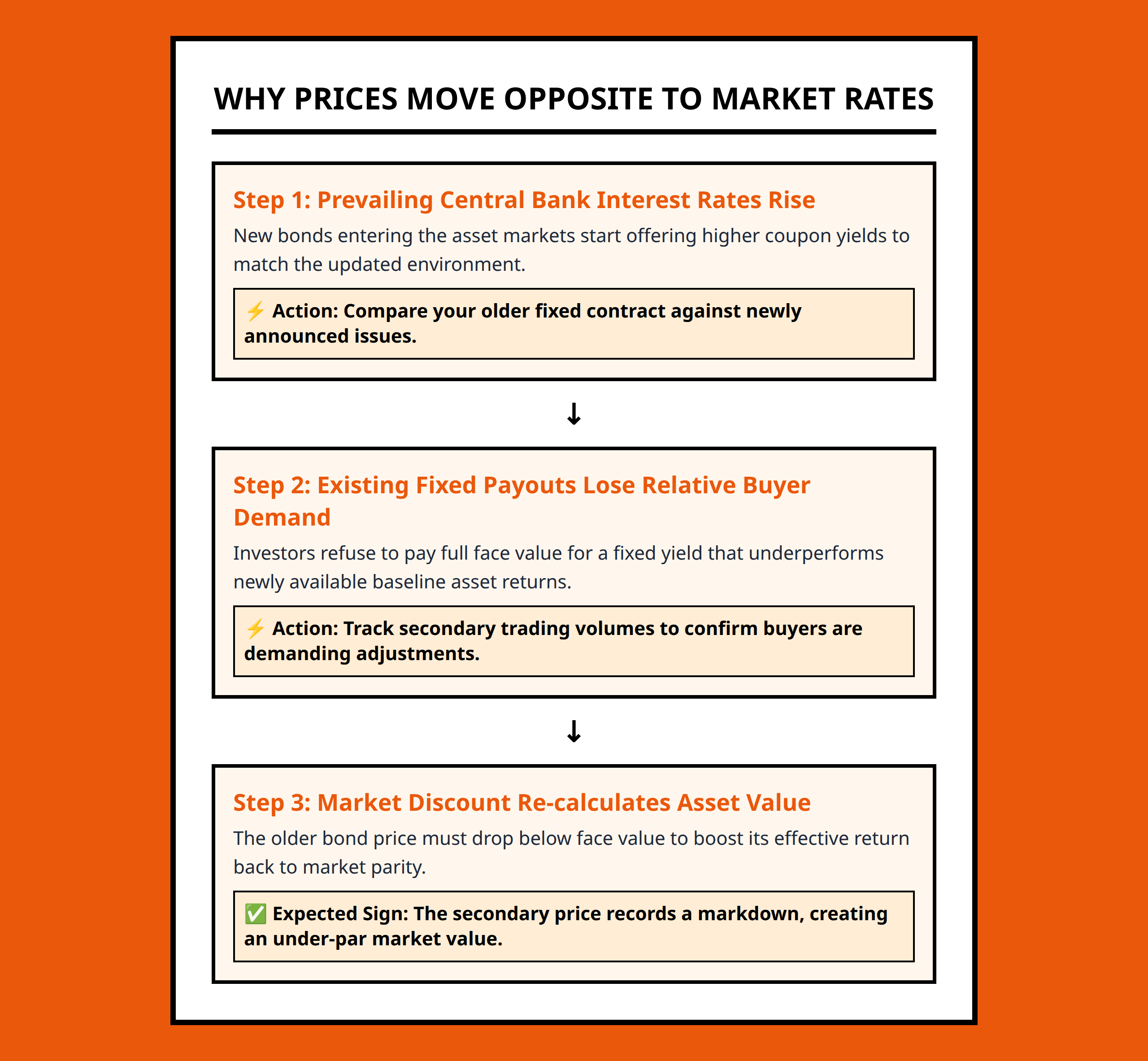

One of the most important ideas in fixed income investing is that bond prices and interest rates move in opposite directions. This is not arbitrary; it is a direct result of how discounting works.

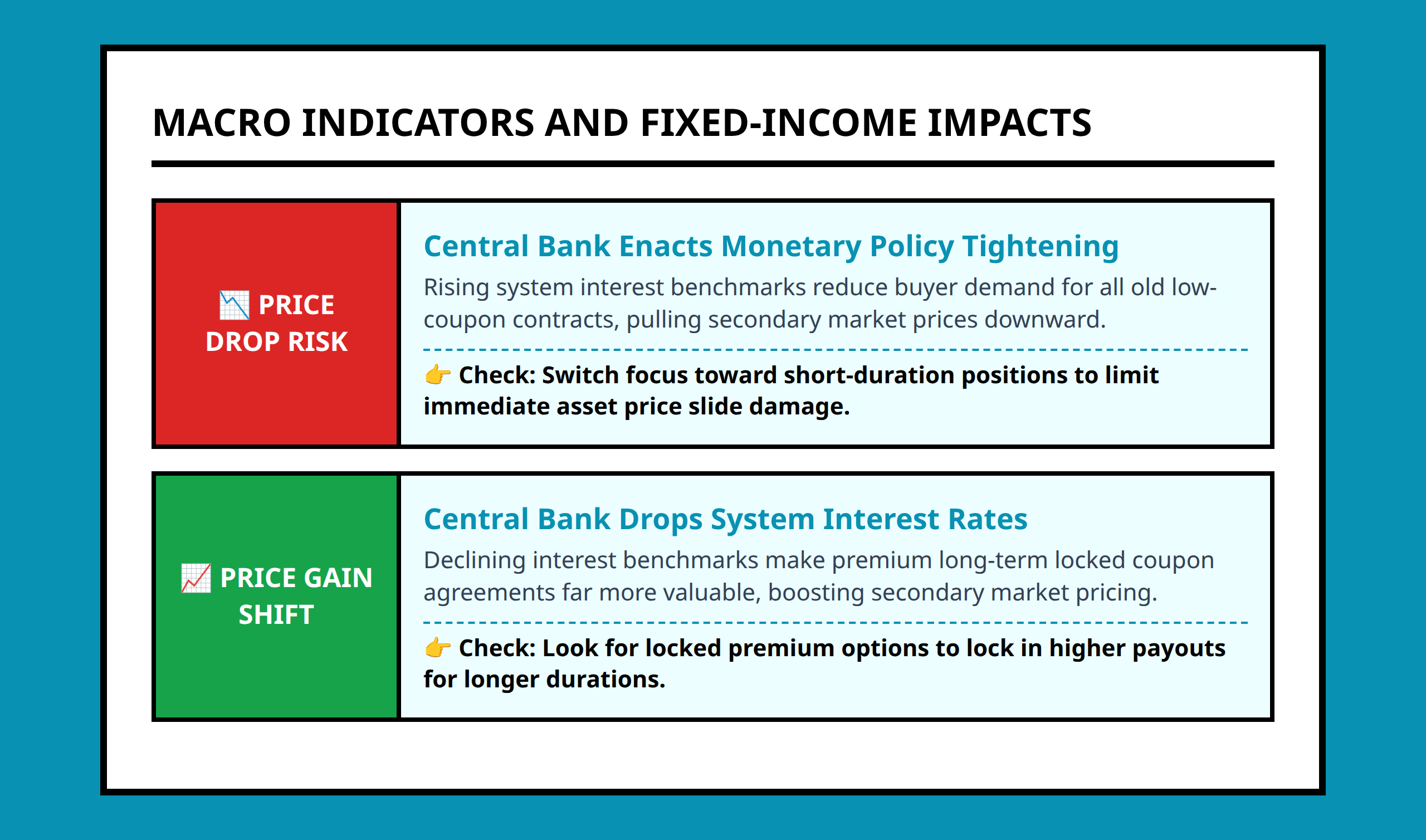

When interest rates rise

When market interest rates increase, new bonds are issued with higher yields. Existing bonds with lower coupon rates become less attractive because their fixed payments are now compared to higher-paying alternatives.

To remain competitive, the price of existing bonds must fall. This price drop increases their effective yield, aligning them with current market conditions.

When interest rates fall

When interest rates decline, existing bonds become more valuable because their fixed coupon payments are now higher than what new bonds offer.

As a result, investors are willing to pay a premium for those higher fixed payments, pushing bond prices upward.

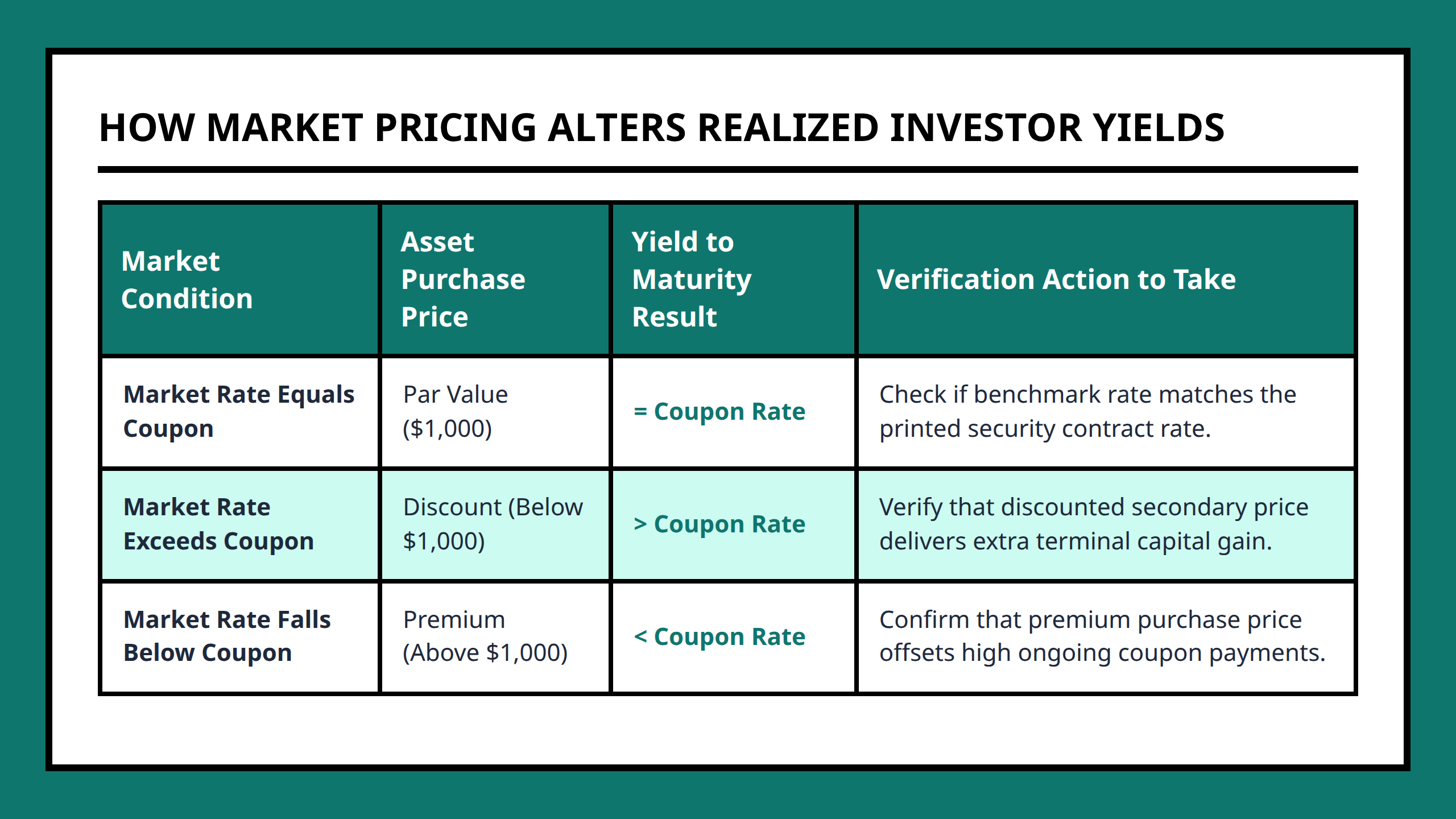

The role of yield to maturity

Yield to maturity represents the total return an investor expects if the bond is held until maturity, assuming all payments are made as scheduled.

It adjusts automatically as bond prices change, ensuring that returns remain aligned with market conditions.

This dynamic relationship between price and yield is what keeps bond markets balanced over time.

Common Bond Investing Mistakes

Even though bond valuation follows a clear logic, investors often make mistakes that lead to misinterpretation of returns and risks.

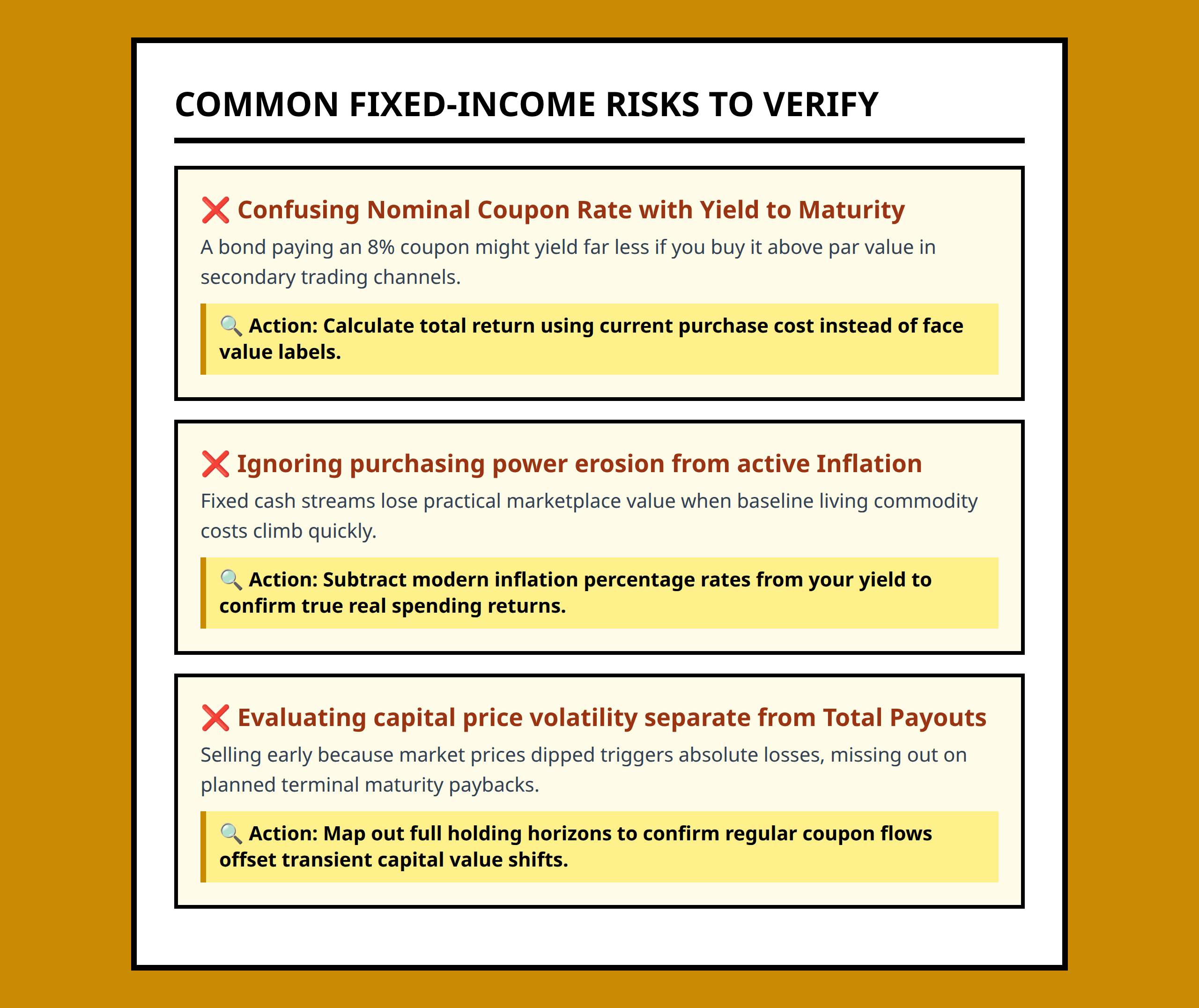

Confusing coupon rate with actual return

One of the most common misunderstandings is assuming that the coupon rate represents the investor’s return. In reality, return depends on the price paid for the bond, not just the coupon amount.

If a bond is purchased above or below face value, the actual yield will differ from the coupon rate.

Ignoring the impact of inflation

Inflation reduces the purchasing power of future bond payments. Even if a bond provides fixed cash flows, those payments may be worth less in real terms if inflation rises.

This makes inflation expectations an important part of bond valuation.

Focusing only on price changes

Some investors focus only on bond price movements and ignore total return, which includes both price changes and coupon income.

A bond may experience price declines but still generate positive total returns through coupon payments.

Underestimating interest rate risk

Longer-term bonds are especially sensitive to interest rate changes. Small shifts in rates can lead to significant price fluctuations.

Failing to account for this risk can lead to unexpected losses in bond portfolios.

Why Bond Valuation Matters in Real Financial Decisions

Bond valuation is not just an academic exercise. It directly affects how investors allocate capital, manage risk, and interpret market movements.

Understanding the relationship between interest rates and bond prices helps investors make more informed decisions about timing, duration, and portfolio structure.

It also provides insight into broader economic conditions. Rising interest rates often reflect changing monetary policy or inflation expectations, which in turn influence bond valuations across the market.

In practice, bond valuation becomes a tool for interpreting both individual investment opportunities and macroeconomic trends.

FAQ

- Bond: A fixed-income instrument where an investor lends money to an issuer in exchange for interest payments and repayment at maturity.

- Coupon: The periodic interest payment made to bondholders.

- Face Value: The amount repaid to the investor when the bond matures.

- Yield to Maturity: The total expected return on a bond if held until maturity.

- Discount Rate: The rate used to calculate the present value of future cash flows.

- Inflation: The general increase in prices that reduces purchasing power over time.

References:

- https://www.investopedia.com/ask/answers/why-interest-rates-have-inverse-relationship-bond-prices/

- https://www.pimco.com/us/en/resources/education/bonds-102-understanding-how-interest-rates-affect-bond-performance

- https://www.schwab.com/learn/story/what-happens-to-bonds-when-interest-rates-rise

- https://www.sec.gov/files/ib_interestraterisk.pdf

- https://www.hartfordfunds.com/dam/en/docs/pub/whitepapers/CCWP142.pdf

- https://www.finra.org/investors/insights/bonds-interest-rate-changes-duration

- https://www.usbank.com/investing/financial-perspectives/market-news/interest-rates-affect-bonds.html

- https://www.fidelity.com/learning-center/investment-products/fixed-income-bonds/bond-prices-rates-yields

- https://www.bluechippartners.com/blog/interest-rates-vs-bond-prices-what-happens-when-rates-change/