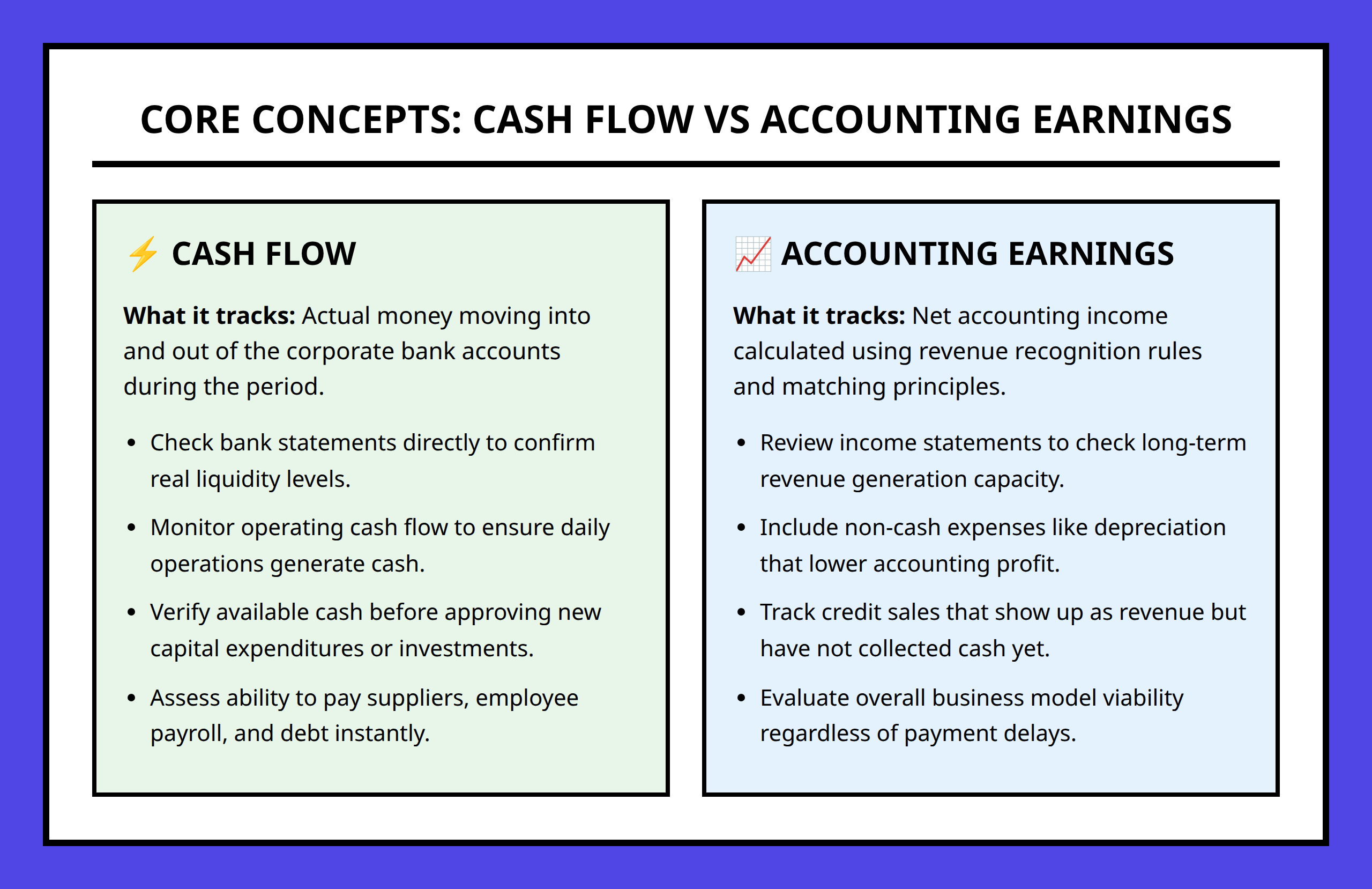

Cash flow measures actual money moving through a business, while earnings are accounting-based measures that may not reflect real liquidity. Understanding the difference is essential because companies can appear profitable on paper but still struggle to survive due to cash shortages.

One of the most common misunderstandings in business is assuming that profitability automatically means financial strength. It feels intuitive: if a company reports strong earnings, it should be healthy. But in practice, financial managers often pay closer attention to cash flow than to reported profits.

This is because earnings are shaped by accounting rules and timing assumptions, while cash flow reflects the actual movement of money. The gap between the two can be large enough to completely change how a company is evaluated. Once you understand this difference, financial statements start to tell a much more realistic story about a business.

In this article, I want to break down why cash flow and earnings often diverge, why that divergence matters, and how professionals use both together to make better decisions.

Takeaways

- Earnings reflect accounting rules, while cash flow reflects real money movement.

- A profitable company can still fail if it lacks sufficient cash.

- Financial managers prioritize cash flow because it determines survival and flexibility.

- Understanding financial statements requires analyzing both earnings and cash flow together.

What Earnings Measure and Their Limitations

Earnings, also known as accounting income, represent a company’s profit over a period of time. They are reported on the income statement and are designed to measure performance using standardized accounting rules.

To understand earnings properly, it helps to look at how they are constructed. Accounting systems rely on principles such as revenue recognition and matching. These rules determine when revenue is recorded and when expenses are recognized, even if cash has not yet changed hands.

This is where the first major difference between earnings and cash flow appears.

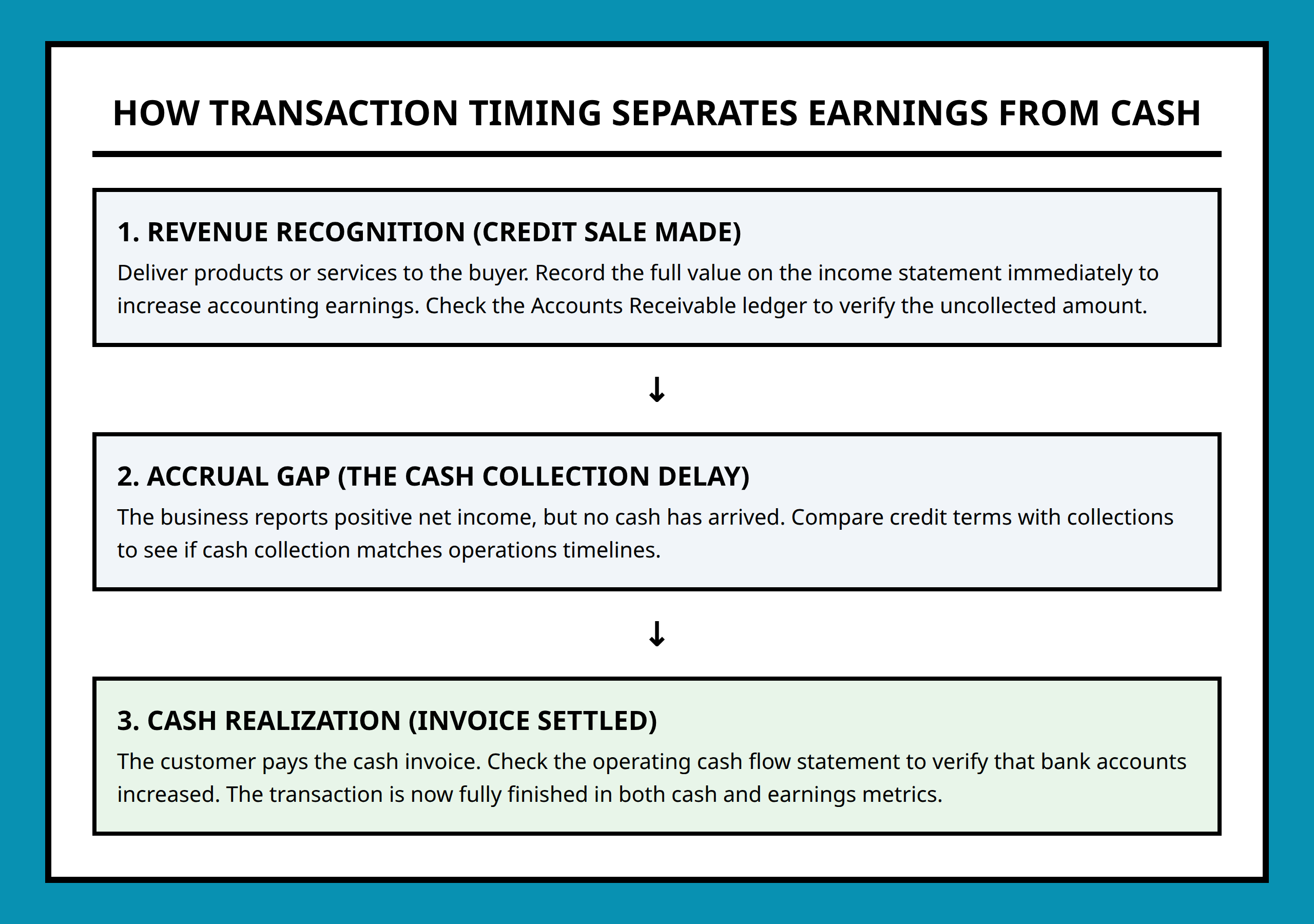

Revenue recognition and timing differences

Revenue is not always recorded when cash is received. Instead, it is often recorded when it is earned. For example, a company might deliver a product today but receive payment weeks or months later. The income is recorded immediately, even though the cash has not arrived.

This timing difference creates a gap between reported earnings and actual cash flow.

Matching principle and expense timing

Expenses are also recorded based on when they are incurred, not necessarily when they are paid. This is called the matching principle, where costs are aligned with the revenues they help generate.

As a result, a company might report expenses before or after cash is actually paid out. This again causes earnings to diverge from real cash movement.

Non-cash expenses and accounting adjustments

Some expenses reduce earnings but do not involve any cash leaving the business. Depreciation is a common example. It reflects the allocation of asset cost over time but does not represent an actual cash payment during the reporting period.

These non-cash expenses can significantly reduce earnings while leaving cash levels unchanged.

Because of these accounting mechanics, earnings are useful for measuring performance but limited when evaluating liquidity and short-term financial health.

Why Cash Flow Is Critical for Business Survival

Cash flow represents the actual movement of money into and out of a business. Unlike earnings, it reflects what the company can actually use to operate, invest, and survive.

This distinction is why financial managers often prioritize cash flow when making decisions.

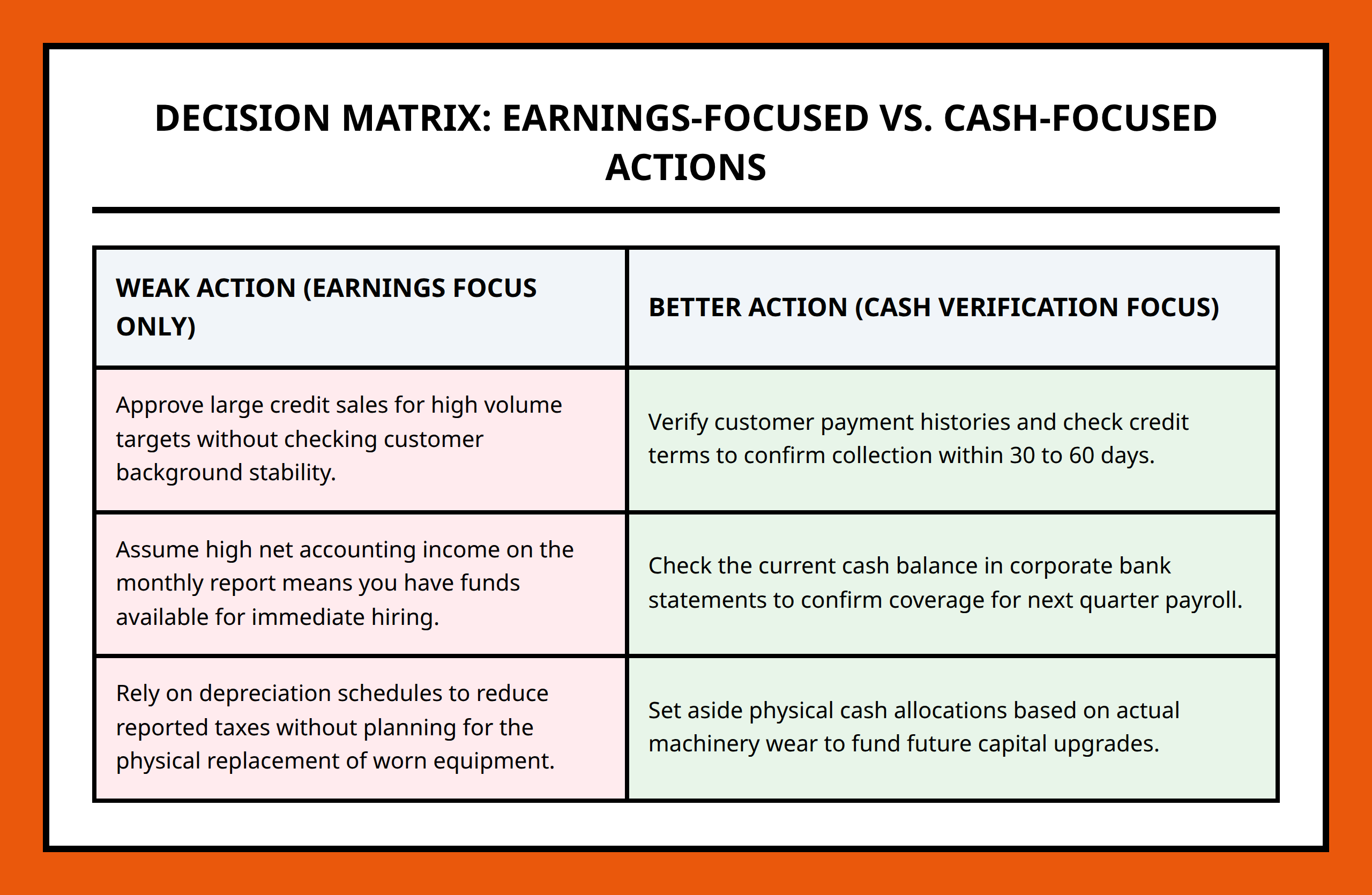

Paying day-to-day obligations

A business must pay employees, suppliers, rent, and other operational costs in cash. Even if the income statement shows strong profits, the company cannot continue operating without enough cash on hand.

This is one of the most important realities of financial management: obligations require cash, not accounting profits.

Funding investments and growth

Companies also need cash to invest in new projects, equipment, and expansion opportunities. These investments are not always reflected immediately in earnings, but they require real liquidity.

A business with strong earnings but weak cash flow may struggle to grow because it lacks the funds to invest.

Meeting debt obligations

Debt payments are another area where cash is essential. Interest and principal repayments must be made in cash, regardless of accounting profit.

If a company cannot generate enough cash flow, it may struggle to meet these obligations even if it appears profitable on paper.

Supporting business flexibility

Cash also provides flexibility. Companies with strong cash positions can respond quickly to opportunities or unexpected challenges. Without cash, even profitable firms may be forced into difficult financial decisions.

This is why cash flow is often considered a more reliable indicator of financial health than earnings alone.

How to Analyze Financial Statements for Better Decisions

Understanding the difference between cash flow and earnings is only the first step. The real value comes from learning how to read financial statements together to get a complete picture of a company’s health.

Reading income statements alongside cash flow statements

The income statement shows earnings, while the cash flow statement shows how cash actually moves through the business. When used together, they help identify whether profits are supported by real cash generation.

A company may report strong earnings but weak operating cash flow. This could signal that profits are tied up in receivables or non-cash adjustments rather than actual cash inflows.

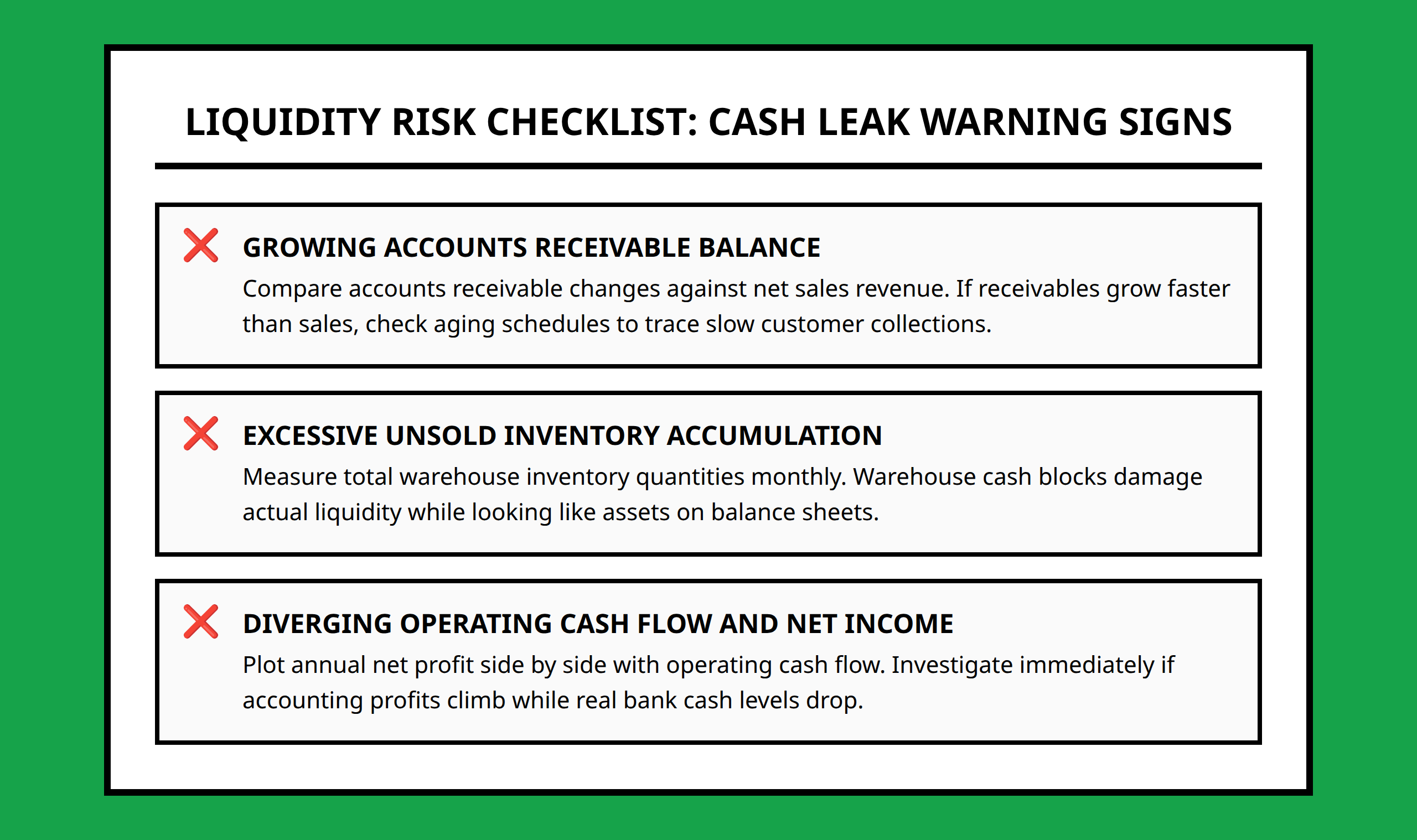

Identifying warning signs in cash flow patterns

One of the key skills in financial analysis is recognizing when cash flow does not match reported earnings. For example, consistently low operating cash flow compared to earnings may indicate inefficiencies in collecting payments or managing expenses.

Over time, this imbalance can create liquidity problems even in otherwise profitable companies.

Evaluating operating cash flow trends

Operating cash flow is especially important because it reflects cash generated from core business activities. Strong and stable operating cash flow is often a sign of a healthy business model.

Analysts often look at trends over time rather than single-period numbers to understand whether a company’s cash generation is improving or weakening.

By focusing on these patterns, decision-makers can avoid being misled by short-term accounting results and instead focus on long-term financial stability.

Why the Difference Between Cash Flow and Earnings Matters

The gap between cash flow and earnings is not just a technical accounting issue. It directly affects how businesses make decisions, allocate resources, and evaluate risk.

A company can look strong on paper while quietly struggling with liquidity. This mismatch is one of the main reasons financial managers rely heavily on cash-based analysis when making decisions.

In practice, cash flow determines whether a business can survive day-to-day operations, while earnings help measure long-term performance. Both are important, but they serve different purposes.

FAQ

- Earnings: Accounting profit measured on the income statement using accrual-based accounting rules.

- Cash Flow: Actual movement of money into and out of a business.

- Operating Cash Flow: Cash generated from core business operations.

- Accrual Accounting: A system that records revenues and expenses when they are earned or incurred, not when cash changes hands.

- Liquidity: A company’s ability to meet short-term financial obligations using available cash.

References:

- https://www.investopedia.com/ask/answers/111714/whats-more-important-cash-flow-or-profits.asp

- https://online.hbs.edu/blog/post/cash-flow-vs-profit

- https://www.extension.iastate.edu/agdm/wholefarm/html/c5-213.html

- https://www.sciencedirect.com/science/article/pii/S0165410198000202

- https://avior.com/insights/economic-and-market-commentary/whats-the-difference-between-cash-flow-and-income-and-why-does-it-matter/

- https://www.debtbook.com/blog/cash-flow-vs-revenue

- https://www.youtube.com/watch?v=y0ElUn3ftcM

- https://www.youtube.com/watch?v=xbasHzq2fL0

- https://www.linkedin.com/posts/chrishervochon_net-income-can-lie-to-you-not-because-your-activity-7418318181846478848-dqd0

- https://www.quora.com/Why-do-we-focus-on-cash-flows-rather-than-accounting-profits-in-making-our-capital-budgeting-decisions-Why-are-we-interested-only-in-the-incremental-cash-flows-rather-than-the-total-cash-flows

- https://www.liveplan.com/blog/managing/cash-vs-profits

- https://shinewingtyteoh.com/cash-flow-more-important-than-profit

- https://www.citizensbank.com/learning/cash-flow-vs-profit.aspx