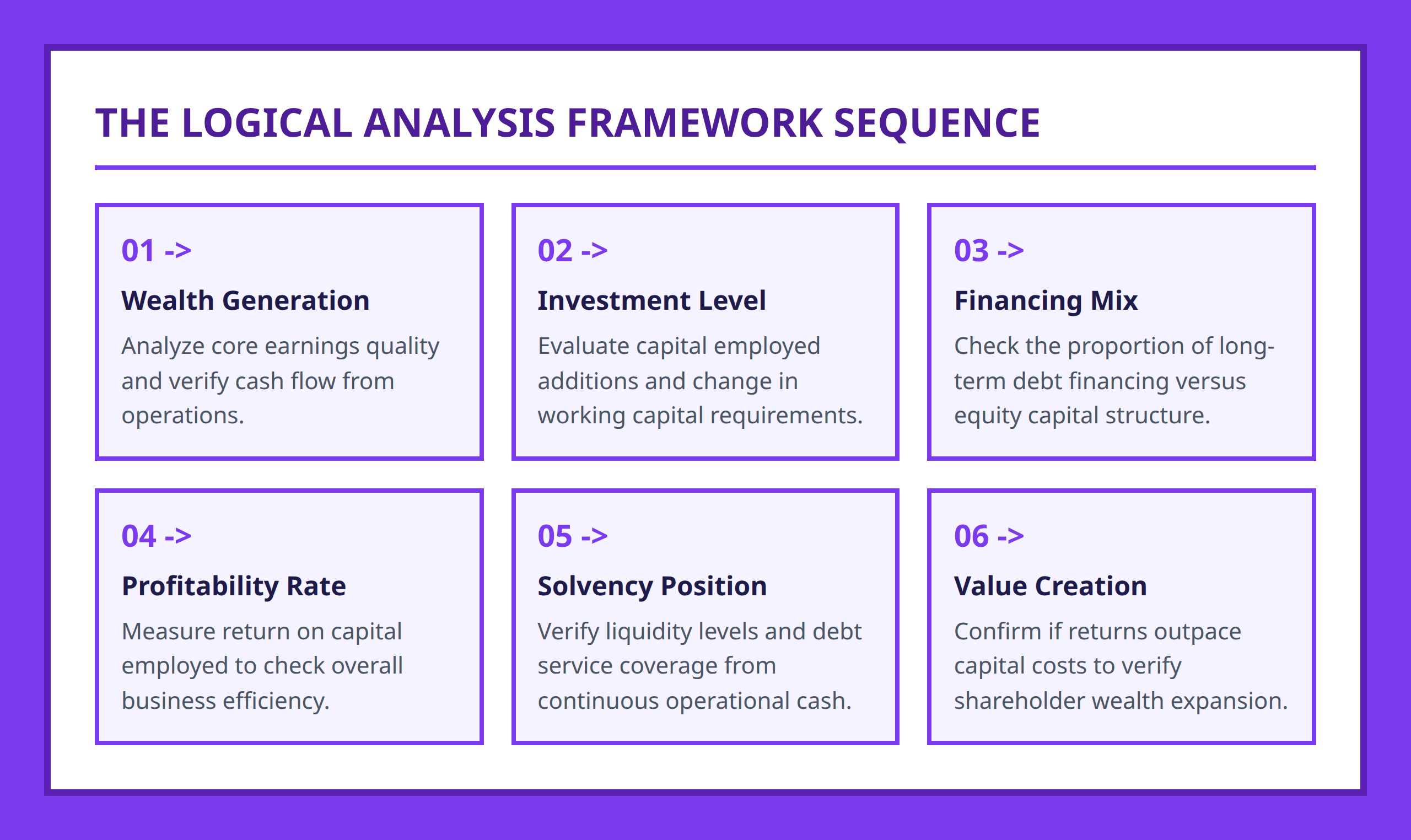

Financial analysis becomes much easier when you stop looking at individual ratios and start following a structured sequence. The most useful approach is to examine how a company generates wealth, invests capital, finances operations, maintains solvency, and ultimately creates value.

Many people open a set of financial statements and immediately get lost. There are income statements, balance sheets, cash flow statements, margins, debt ratios, returns on capital, and dozens of other metrics competing for attention.

I find that the real challenge is not understanding individual numbers. It is understanding how those numbers connect. Strong financial analysis follows a logical path, where each step helps explain the next one.

Takeaways

- Start with cash flow, earnings, and capital employed before looking at advanced ratios.

- Analyze investment and financing decisions separately before judging performance.

- Profitability and solvency answer different questions and should never be confused.

- The final objective is determining whether a company creates value while remaining financially sustainable.

Start With Cash Flow, Earnings, and Capital Employed

The first step is understanding how the company generates and uses financial resources.

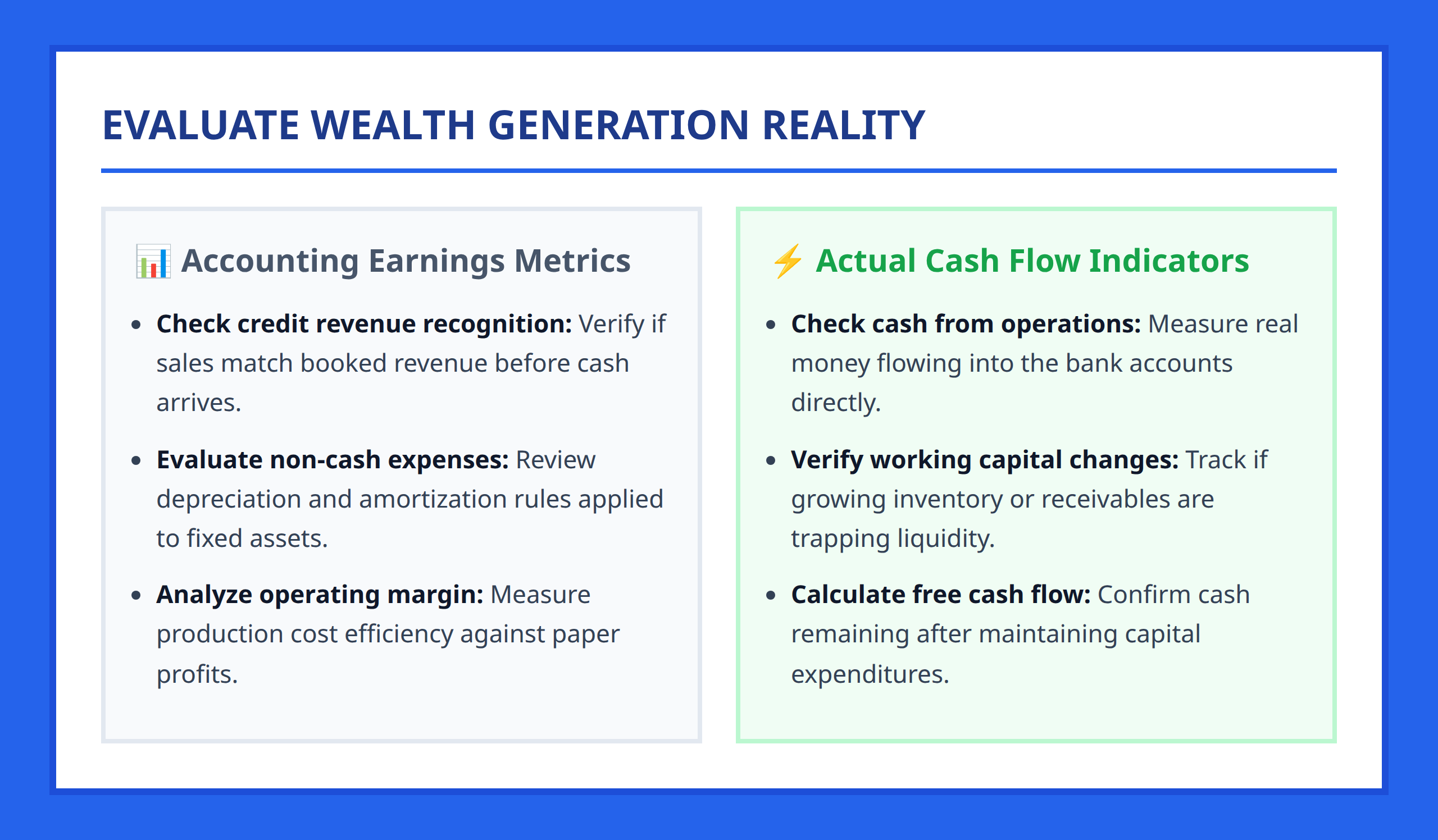

Cash flow shows the movement of money through the business. It reveals whether operations generate cash, whether investments consume cash, and how financing activities support or absorb resources. Cash flow often exposes realities that accounting earnings alone may not reveal.

Earnings provide another perspective. They show whether the business is creating wealth through its operations. Earnings help explain performance, but they should always be interpreted alongside cash flow because accounting results and cash generation can differ significantly.

Capital employed adds an important layer. It represents the resources committed to operating the business. Looking at earnings without considering how much capital was required to generate them can produce misleading conclusions.

An illustrative example is a company reporting strong earnings growth while consuming increasing amounts of cash and requiring substantial additional investment. The earnings may look attractive, but the broader financial picture may be less impressive once capital requirements are considered.

Analyze Investment and Financing Decisions

The next step is understanding where resources go and how those resources are funded.

Companies invest capital through working capital requirements and longer-term capital expenditures. These decisions shape future growth, operating capacity, and cash generation potential.

Working capital analysis helps explain how efficiently a company manages inventories, receivables, and payables. Changes in working capital can significantly influence cash flow even when reported earnings remain stable.

Capital expenditure analysis focuses on long-term investments. Businesses must continually decide how much to invest in maintaining or expanding operations. These investments often determine future profitability and competitiveness.

Financing analysis examines how these investments are funded. Companies typically rely on a combination of internally generated cash, debt, and equity capital.

| Analysis Area | Main Question |

|---|---|

| Working Capital | How efficiently are short-term resources managed? |

| Capital Expenditures | How much is being invested for future operations? |

| Debt Financing | How dependent is the company on borrowed funds? |

| Equity Financing | How much capital comes from shareholders? |

When evaluating a business, I find it useful to ask a simple question: is growth being supported primarily by strong operations or by increasing financial commitments? The answer often reveals a great deal about financial quality.

Assess Profitability, Solvency, and Value Creation

Once operations, investments, and financing have been analyzed, the focus shifts to overall performance.

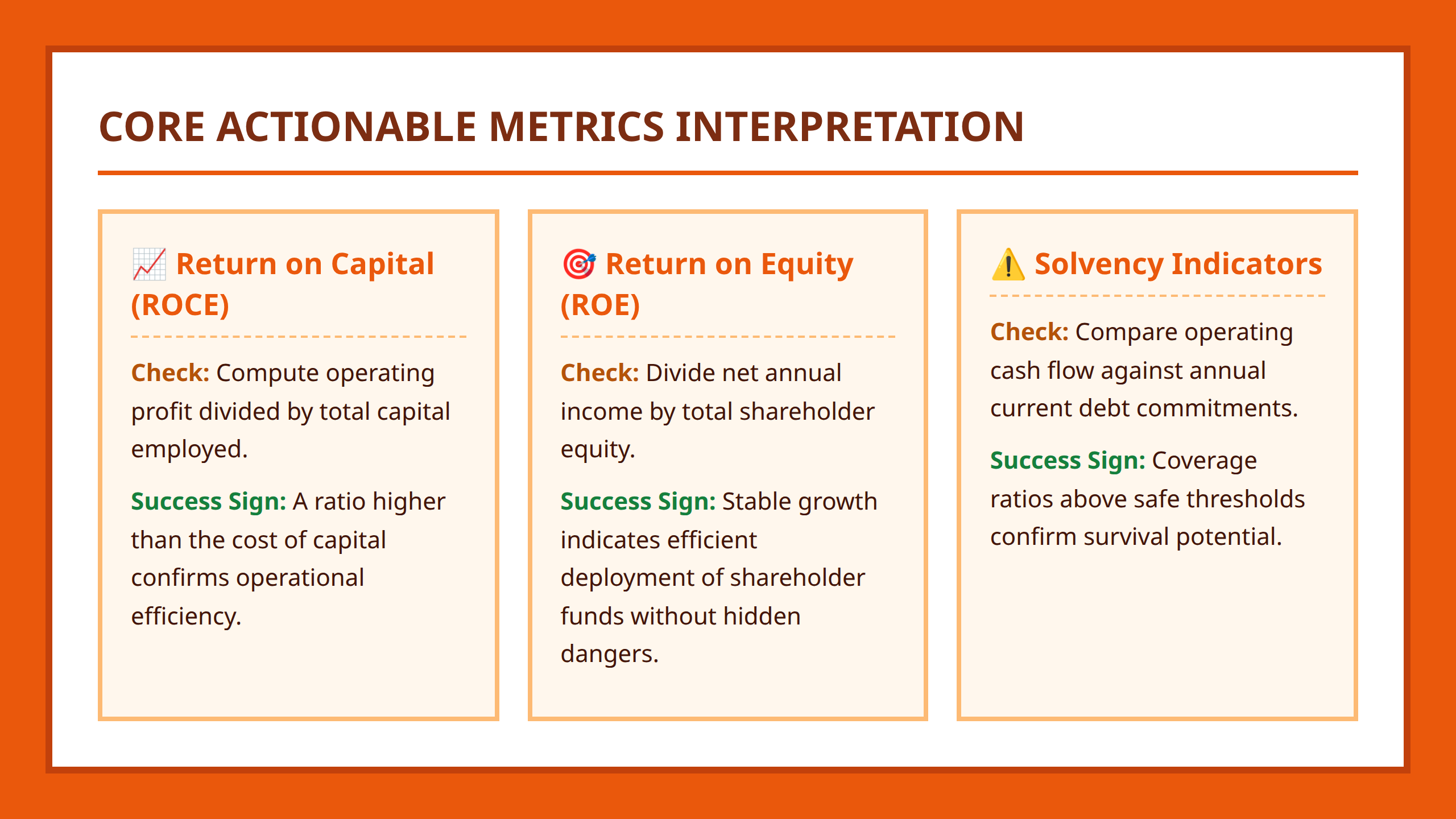

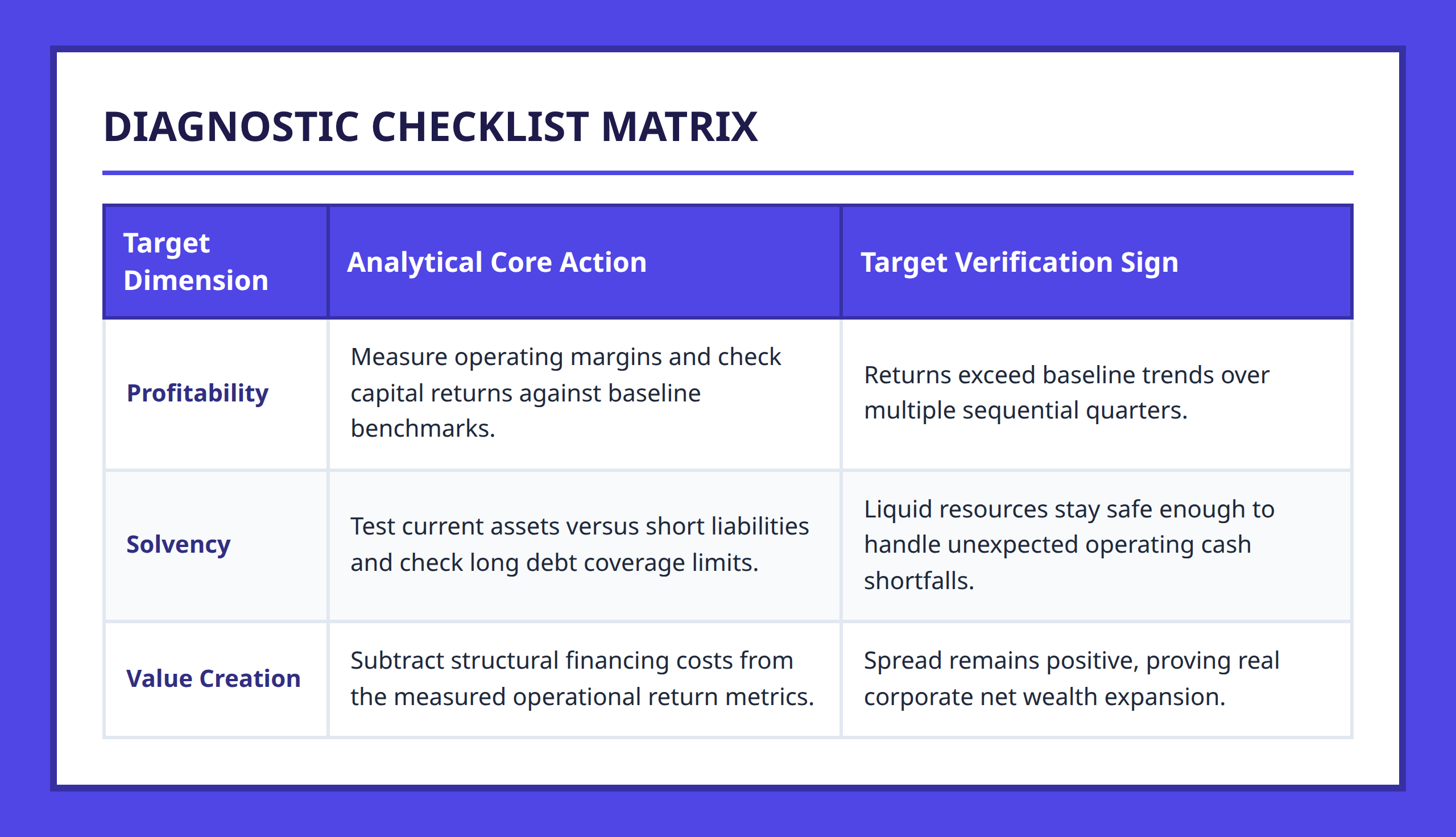

Profitability analysis measures how effectively the company converts resources into returns. Metrics such as return on capital employed and return on equity help connect profits to the resources required to generate them.

Return on capital employed is particularly useful because it evaluates performance relative to the capital invested in operations. It helps answer whether management is generating sufficient returns from the resources under its control.

Solvency analysis addresses a different question. Instead of asking whether the company is profitable, it asks whether the company can remain financially viable over time. A profitable company can still face difficulties if its financial obligations exceed its ability to meet them.

The strongest analyses combine profitability and solvency rather than focusing on one at the expense of the other. High returns become less meaningful if financial stability is weak. Likewise, strong solvency alone does not guarantee value creation.

The final objective is determining whether the company creates value. A company creates value when it generates returns that justify the capital invested and the risks assumed. This moves analysis beyond isolated ratios and toward a broader assessment of business quality.

A Practical Sequence for Financial Analysis

Answer first: follow a consistent order.

- Understand cash flow generation.

- Evaluate earnings quality.

- Assess capital employed.

- Review working capital and capital expenditures.

- Analyze financing sources.

- Measure profitability.

- Evaluate solvency.

- Determine whether value is being created.

This sequence prevents one of the most common mistakes in analysis: jumping directly to performance ratios without understanding the economic and financial foundations behind them.

FAQ

The Most Useful Habit in Financial Analysis

The best analysts rarely start with ratios. They start with understanding the business’s financial mechanics.

When you consistently move from cash flow to earnings, from investments to financing, and from profitability to solvency, financial statements begin to tell a coherent story. The next time you analyze a company, resist the temptation to chase individual metrics and instead follow the sequence. The quality of your conclusions will usually improve immediately.

- Cash Flow: The movement of cash into and out of a business through operations, investments, and financing activities.

- Earnings: The accounting measure of profit generated during a period.

- Capital Employed: The financial resources invested in operating a business.

- Working Capital: Short-term operating resources such as inventories, receivables, and payables.

- Return on Capital Employed (ROCE): A measure of how effectively a company generates returns from invested capital.

- Return on Equity (ROE): A measure of profitability relative to shareholders’ equity.

- Solvency: A company’s ability to meet its long-term financial obligations.

- Value Creation: Generating returns that exceed the cost and risk associated with invested capital.