The time value of money explains why €100 today is not the same as €100 in the future. Money can grow when invested, and future cash is uncertain. Because of this, all financial decisions depend on converting future cash flows into present value using discounting, compounding, and risk adjustment.

At first glance, the idea feels almost too simple: money today is better than money later. But once you start applying it to real decisions—like investments, loans, or project planning—it becomes clear that this principle quietly drives almost everything in finance.

What makes it powerful is not just time, but uncertainty. Future cash flows are not guaranteed, and that changes how we value them. This is where tools like compounding and discounting become essential, turning uncertain future outcomes into comparable present values.

Takeaways

- Money today is worth more because it can be invested and grow over time.

- Future cash must be discounted to compare it fairly with present money.

- Risk changes valuation—uncertain cash flows are treated differently than guaranteed ones.

- Financial decisions rely on translating all cash flows into present value terms.

Why Money Has a Time Value

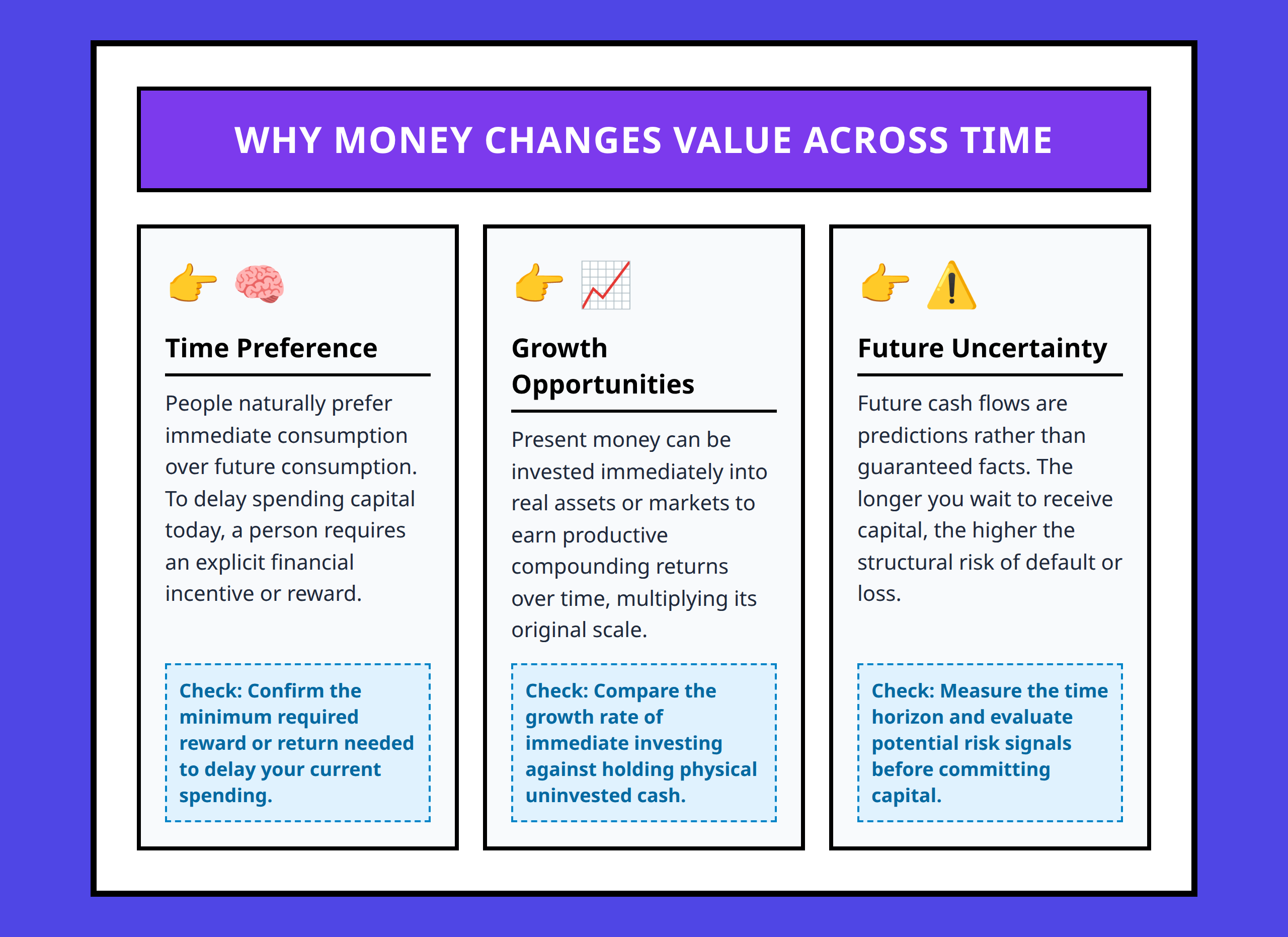

The value of money changes over time because people prefer consumption now rather than later, and because money can be used productively. These two forces—time preference and investment opportunity—form the foundation of the time value of money.

From a human perspective, waiting often feels costly. If you receive €100 today, you can spend it, save it, or invest it. If you receive it a year later, you lose all those options during that time. That lost flexibility has value.

At the same time, money itself can generate more money. For example, if you invest €100 today at a 10% annual return, it becomes €110 after one year. That €10 gain is the reward for giving up immediate consumption and taking advantage of productive opportunity.

There is also uncertainty. Future money is not only delayed—it is also less certain. Even if someone promises you €100 next year, there is always risk that the payment may not happen as expected. This combination of delay and uncertainty is why future cash is discounted.

Compounding and Discounting in Practice

To compare money across time, finance uses two opposite but connected tools: compounding and discounting.

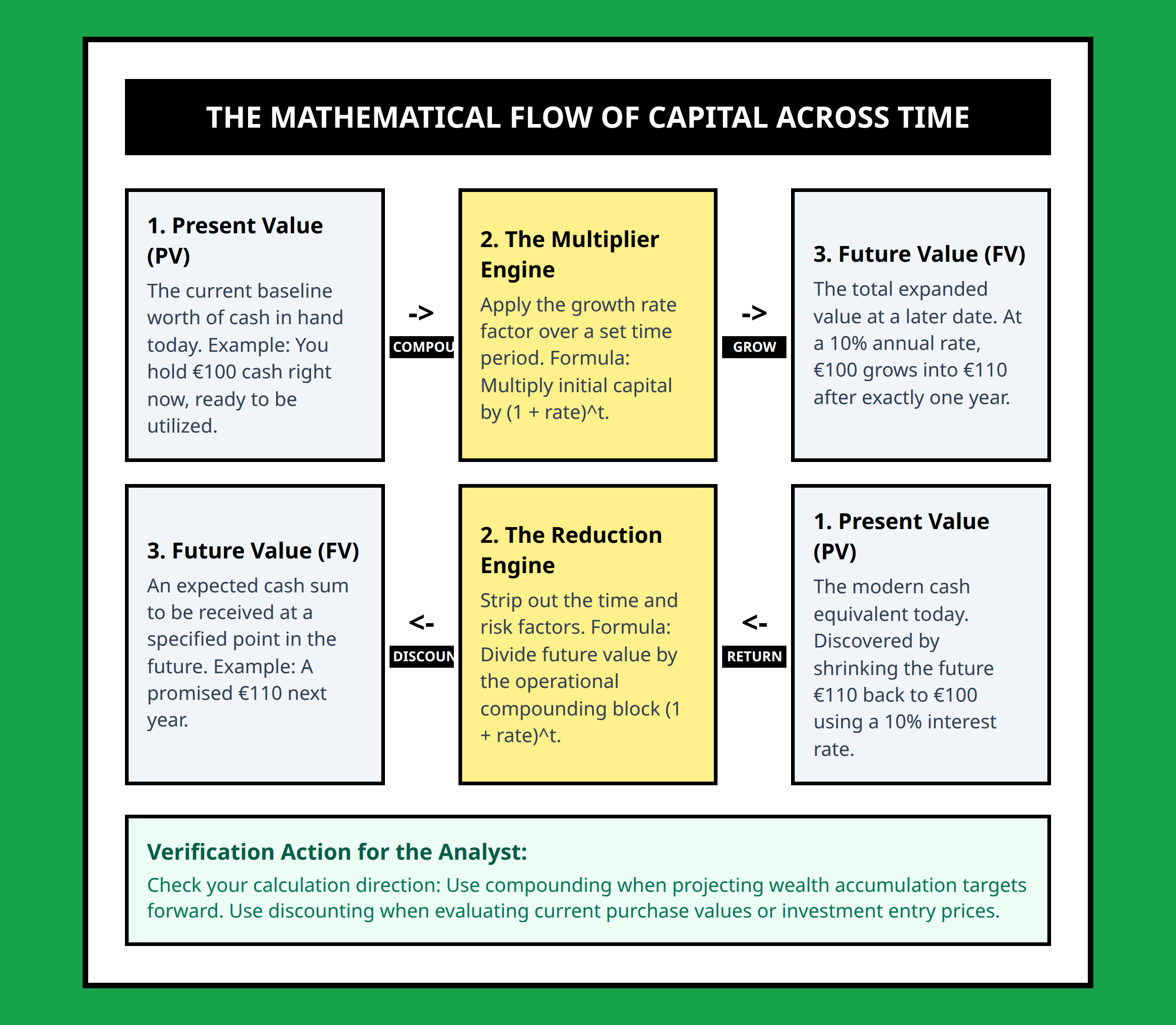

Compounding answers the question: what will today’s money be worth in the future? Discounting answers the opposite: what is future money worth today?

Let’s start with compounding. If you invest €100 at a 10% annual interest rate, the value after one year becomes €110. The formula behind this is simple:

Future Value = Present Value × (1 + interest rate)

So €100 × (1 + 0.10) = €110. If you extend this over multiple years, interest begins to accumulate on interest itself. This is what makes long-term investing powerful.

Now flip the perspective. Suppose someone promises to pay €110 next year. That does not automatically mean it is worth €110 today. To find its present value, we “discount” it using the risk-free interest rate:

Present Value = Future Cash Flow ÷ (1 + discount rate)^t

If the discount rate is 10% and the time is one year, €110 next year is worth €100 today. This is not an arbitrary adjustment—it reflects the fact that €100 today could already be invested and grown.

Without this adjustment, financial decisions would be misleading. A project that pays €110 in one year and costs €100 today is not automatically profitable unless we account for time properly.

Valuing Risky Cash Flows

Real financial decisions rarely involve guaranteed outcomes. Most future cash flows are uncertain, which changes how we value them. Instead of a single number, we think in terms of possible outcomes and probabilities.

For example, imagine a project that could generate €100 or €200 in the future, each with a 50% probability. The expected value is calculated as:

0.5 × 100 + 0.5 × 200 = 150

This €150 is not guaranteed—it is a weighted average of possible outcomes. This is the starting point for valuing risky cash flows, but it is not enough on its own.

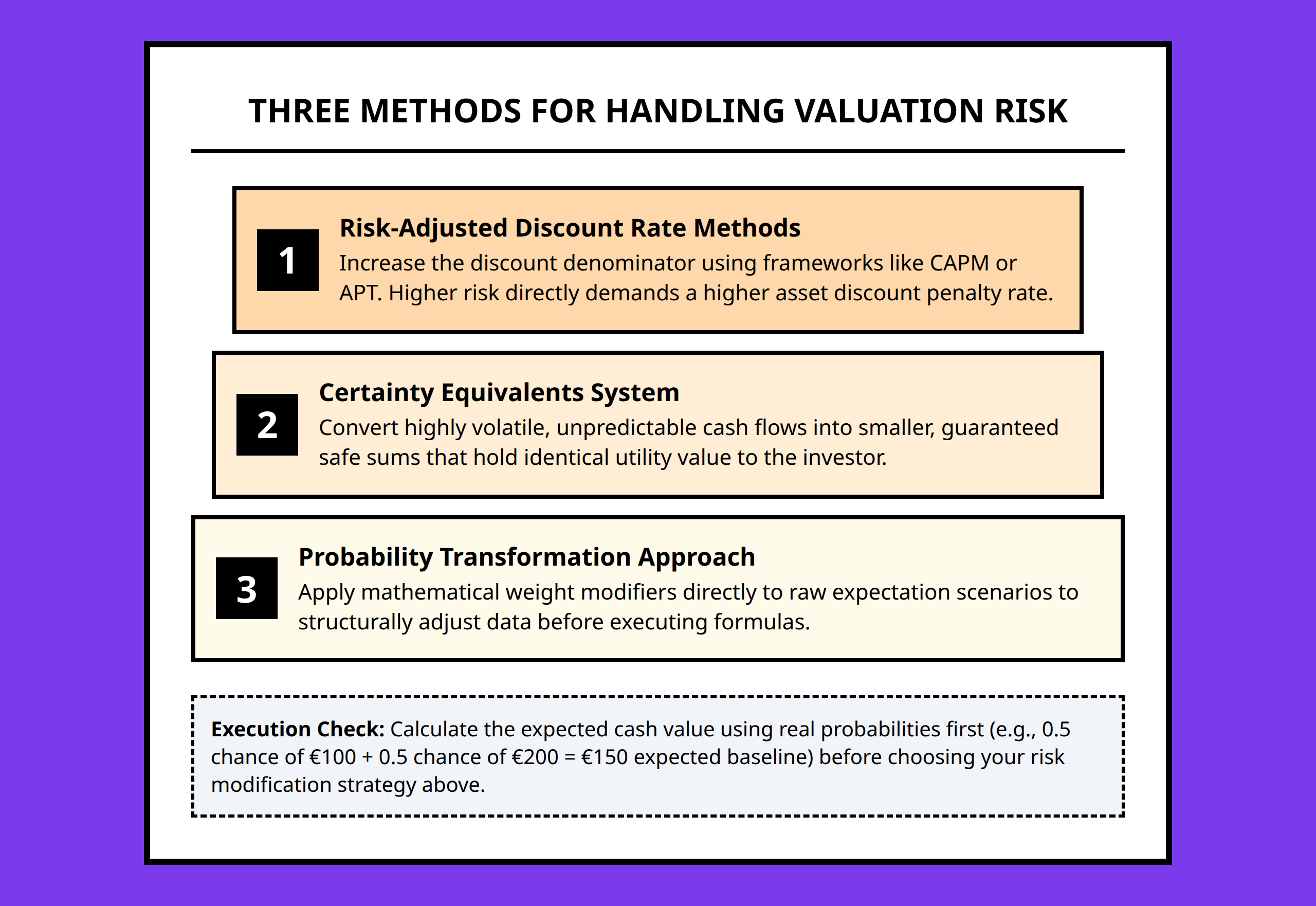

Risk matters. Two projects with the same expected value may have very different levels of uncertainty. Finance handles this in three main ways.

First, the risk-adjusted discount rate. Here, risky cash flows are discounted more heavily than safe ones. Models like CAPM or APT help determine how much extra return investors require for taking risk.

Second, certainty equivalents. Instead of adjusting the discount rate, we adjust the cash flow itself. We ask: what guaranteed amount today would be equivalent to this risky future payoff?

Third, probability transformation. This method changes the way probabilities are used in valuation, embedding risk directly into the calculation framework. One well-known approach uses risk-neutral probabilities in derivative pricing.

Each method leads to the same goal: turning uncertainty into a single present value that can guide decisions.

Why Present Value Is the Core of Financial Decisions

Once you understand compounding, discounting, and risk adjustment, a wide range of financial problems becomes easier to interpret. Whether you are evaluating a project, a stock, or a contract, the logic is the same: translate future outcomes into today’s terms.

This is why valuation is not just a technical tool—it is a decision framework. A project is not valuable because of what it earns in total, but because of what those earnings are worth today after adjusting for time and uncertainty.

In practice, this means even simple decisions require careful thinking. For example, receiving €1,000 in five years is not comparable to €1,000 today without discounting. And a risky €1,000 promise is not the same as a guaranteed one, even if the numbers match on paper.

The discipline of finance is built on this idea: consistent comparison requires a common scale, and that scale is present value.

Common Mistakes When Thinking About Money Over Time

One common mistake is ignoring time altogether. People often compare money amounts directly without adjusting for when they occur. This leads to overestimating the value of delayed payments.

Another mistake is ignoring risk. A future payment that is uncertain is often treated as if it were guaranteed. In reality, uncertainty reduces value, even if the expected amount looks attractive.

Finally, many people misunderstand interest rates. A rate is not just a number—it is a bridge between time periods. It determines how much future money is worth today and how much today’s money can grow in the future.

FAQ

Key Terms Explained

- Time value of money: The principle that money today is worth more than the same amount in the future due to earning potential and uncertainty.

- Discounting: The process of converting future cash flows into present value using an interest rate.

- Compounding: The process of growing present money into future value by earning interest over time.

- Present value: The current worth of future cash flows after adjusting for time and risk.

- Risk-free interest rate: The theoretical return of an investment with no uncertainty, used as a baseline in valuation.

Before making any financial decision, the key question is simple: what are the future cash flows really worth today once time and risk are fully accounted for?

References:

- https://www.investopedia.com/terms/d/dcf.asp

- https://online.hbs.edu/blog/post/discounted-cash-flow

- https://www.investopedia.com/terms/t/timevalueofmoney.asp

- https://www.researchgate.net/publication/358226703_Time_Value_of_Money_and_Discounted_Cash_Flow_Methods

- https://www.treasurers.org/hub/treasurer-magazine/masterclass-discounted-cash-flow

- https://www.chase.com/business/knowledge-center/manage/discounted-cash-flow-valuation

- https://sbpartners.ca/discounted-cash-flow-an-introduction/

- https://www.youtube.com/watch?v=tKUhV40LFgc

- https://www.linkedin.com/posts/financial-modeling-world-cup_valuationmethods-activity-7450136145490874368-jag5

- https://www.youtube.com/watch?v=V1OCkIcIEZI

- https://pressbooks.pub/fundamentaloffinance/chapter/chapter-5-time-value-of-monday-valuing-cash-flow-streams/

- https://www.linkedin.com/posts/compounding-dividends_most-investors-talk-about-stocks-few-take-activity-7469984194459324417-joKH

- https://www.linkedin.com/posts/jason-lum7_lets-walk-through-a-dcf-with-a-simple-example-activity-7457795070633607168-cXkL

- https://www.linkedin.com/posts/compounding-quality_discounted-cash-flow-dcf-explained-activity-7441365179524673536-cu-N

- https://www.linkedin.com/posts/corporate-finance-career®_how-dcf-works-credits-to-bojan-radojicic-activity-7452989729232535552-2Yw9