CAPM shows that expected return depends only on systematic risk (beta), not total risk, because diversification removes firm-specific uncertainty. Portfolio theory explains how combining assets changes risk in ways that individual assets cannot explain on their own.

Most beginners in investing start with the wrong assumption: that each asset has its own “risk level” and expected return, independent of everything else. But financial markets don’t work that way. Once assets are combined into portfolios, their interactions matter more than their individual behavior.

This is where portfolio theory and CAPM change the entire picture. They show that risk is not a single number attached to an asset. Instead, risk is something that emerges from how assets move together. And once you understand that, the idea of “safe” or “risky” stocks becomes much more subtle than it first appears.

Takeaways

- Risk must be understood at the portfolio level, not the individual asset level.

- Diversification removes unsystematic (firm-specific) risk but not market-wide risk.

- CAPM links expected return only to systematic risk measured by beta.

- Real market returns show noise and dispersion around theoretical predictions.

Diversification and the Logic of Portfolio Theory

Portfolio theory starts with a simple but powerful idea: combining assets changes risk in a way that single assets cannot explain. When you hold only one stock, you are exposed to everything that affects that company. But when you hold many assets, some risks cancel out.

This cancellation effect is called diversification. It works because not all risks move in the same direction. One company might perform poorly due to internal issues, while another performs well due to different conditions. When combined, these movements partially offset each other.

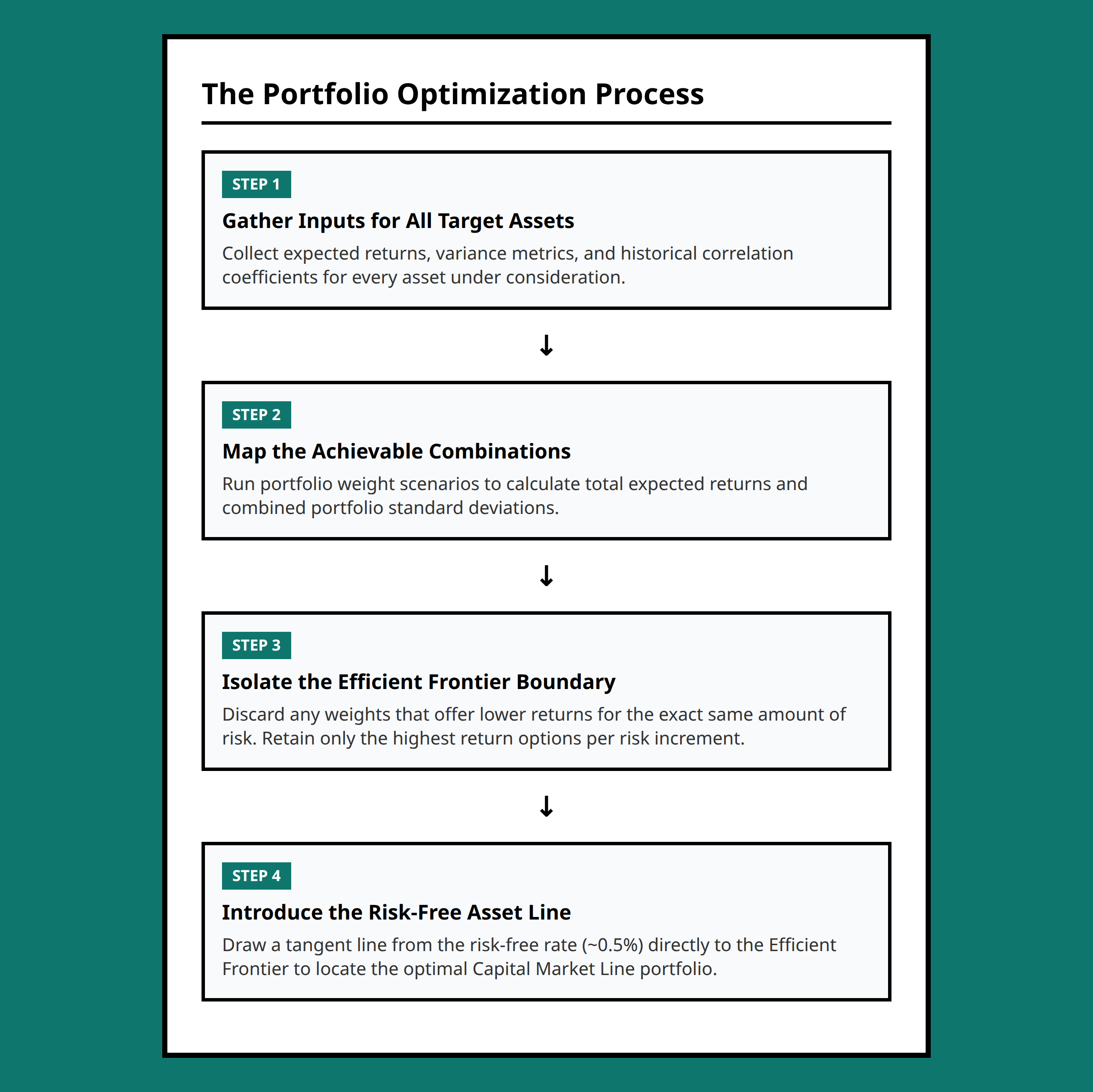

A key concept here is the efficient frontier. This is the set of portfolios that offers the highest expected return for a given level of risk. Any portfolio below this frontier is inefficient because you could either earn more return for the same risk or reduce risk for the same return.

For example, imagine a simple portfolio of two stocks: one technology company and one utility company. The technology stock might have high volatility, while the utility stock is more stable. When combined in different proportions, the overall risk of the portfolio changes in a non-linear way. Some combinations reduce risk more effectively than others, and the efficient frontier captures those best combinations.

This is a fundamental shift in thinking: risk is not something you measure once per asset. It is something you design through portfolio construction.

The Capital Asset Pricing Model (CAPM)

Once portfolio theory explains how risk behaves in groups, CAPM explains how markets price that risk. The central idea is simple: investors are only rewarded for taking on risk that cannot be diversified away.

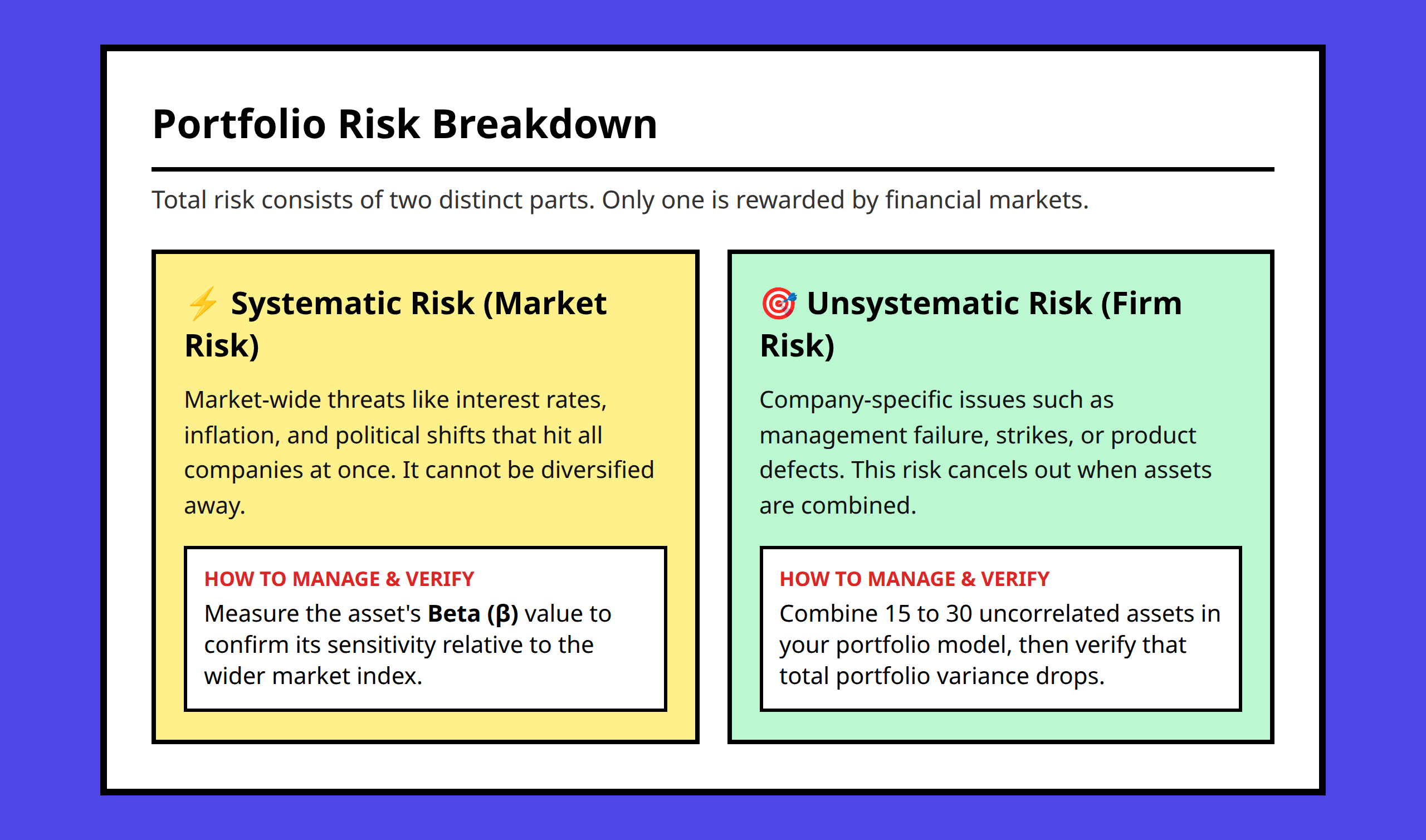

This type of risk is called systematic risk, and it is measured by a factor called beta. Beta tells you how sensitive an asset is to movements in the overall market.

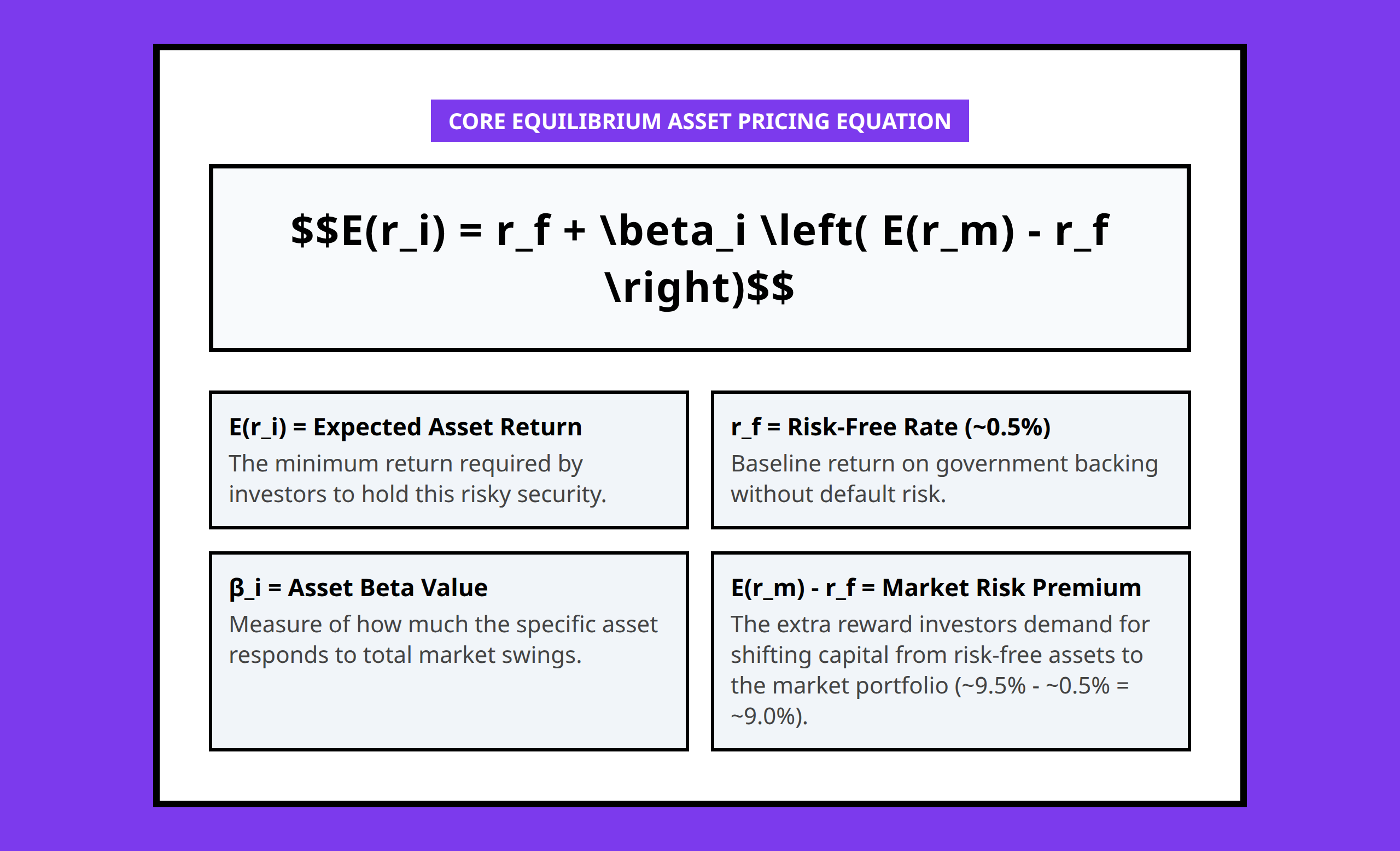

The CAPM equation summarizes the relationship between risk and expected return:

E(ri) = rf + (E(rm) − rf)βi

In this formula, rf is the risk-free rate, E(rm) is the expected market return, and βi is the asset’s beta. The difference (E(rm) − rf) is the market risk premium, which compensates investors for taking systematic risk.

To make this concrete, consider a simplified example from real market assumptions. Suppose the risk-free rate is around 0.5%, and the expected market return is around 9.5%. The market risk premium is therefore 9%.

If a stock has a beta of 1.2, its expected return becomes:

0.5% + (9% × 1.2) = 11.3%

This means investors expect higher returns only because the stock moves more strongly than the overall market. If beta were 0.8, the expected return would be lower, because the stock is less sensitive to market swings.

What matters here is not the total risk of the stock, but how it contributes to the risk of a well-diversified portfolio. That is the key shift CAPM introduces.

Why Only Systematic Risk Matters in Pricing

One of the most important insights in modern finance is that not all risk is priced. If a risk can be eliminated by diversification, investors will not demand extra return for holding it.

This is where the distinction between systematic and unsystematic risk becomes essential. Systematic risk comes from broad market forces—economic conditions, interest rates, or global shocks. Unsystematic risk comes from individual companies or industries.

For example, a factory fire at a single company is unsystematic risk. It affects that company but not the entire market. In a diversified portfolio, such risks largely cancel out. Because of that, markets do not reward investors for bearing them.

Only systematic risk remains after diversification. CAPM uses beta to capture exactly this remaining exposure. A high-beta stock contributes more to portfolio volatility than a low-beta stock, even if both have similar standalone risk.

This is why two stocks with the same total volatility can still have very different expected returns. The structure of risk matters more than its size.

Efficient Frontier and Capital Market Line

When you combine risky assets with a risk-free asset, a new structure appears: the Capital Market Line (CML). This line represents portfolios that optimally mix risk-free and risky investments.

The CML shows that investors can choose their level of risk by adjusting their allocation, rather than picking individual assets. A conservative investor might hold mostly risk-free assets, while an aggressive investor might borrow at the risk-free rate and invest more heavily in the market portfolio.

The result is that portfolio choice becomes a trade-off between risk and return along a straight line, rather than a complex selection of individual securities.

This reinforces the main message of portfolio theory: what matters is not which assets you pick, but how you combine them.

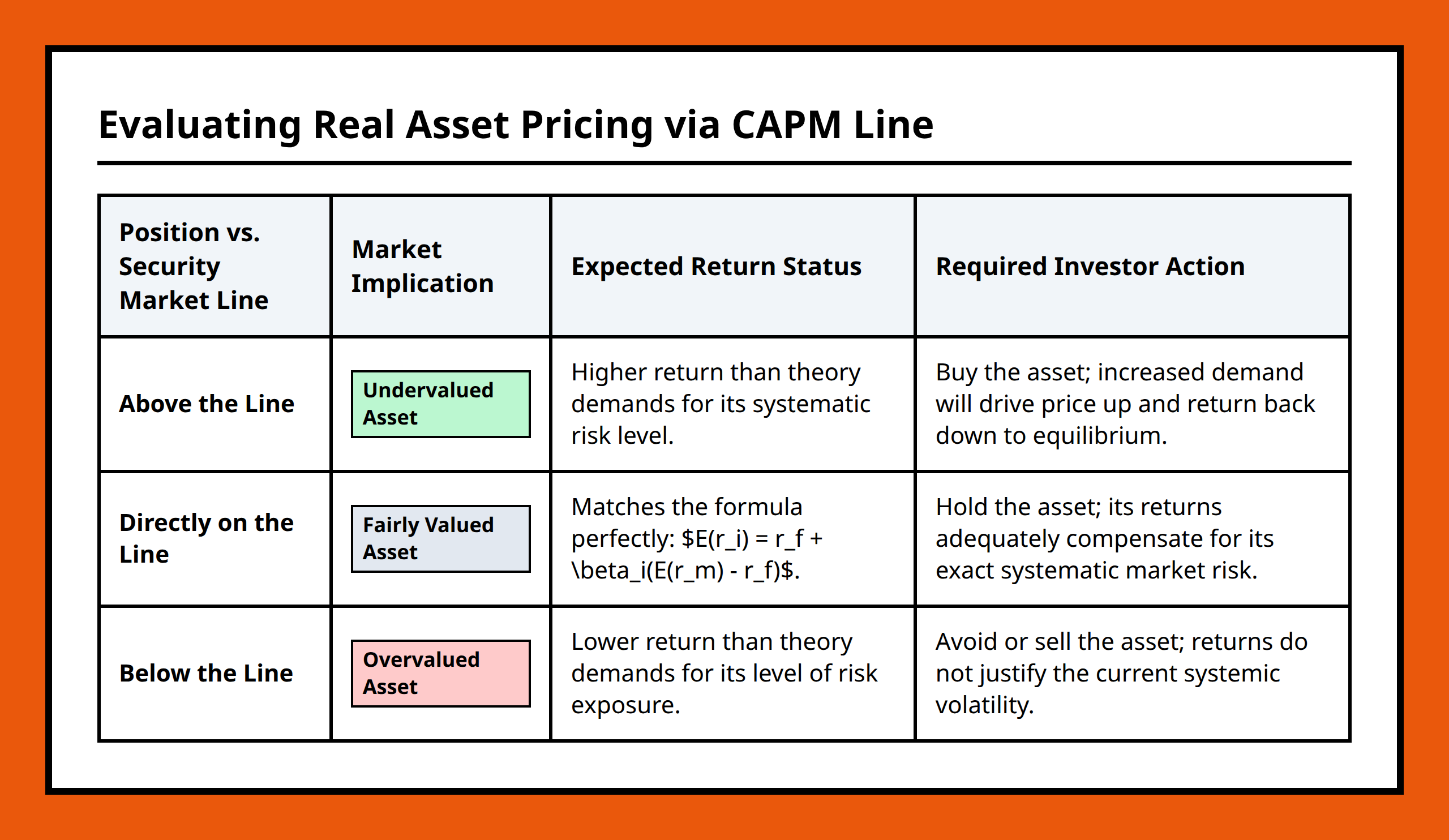

Why Real Markets Do Not Follow CAPM Perfectly

Although CAPM provides a clean theoretical relationship, real market data does not perfectly align with it. Returns show significant dispersion around the predicted line.

In practice, two stocks with similar beta values may still have very different realized returns. This does not necessarily mean the model is wrong. Instead, it reflects the fact that financial markets are noisy systems where many unpredictable factors influence prices.

Even when CAPM was first tested, it was found that it explains a large portion of variation in returns, but not all of it. There is always residual variation that cannot be fully captured by beta alone.

This is an important reminder: financial models are not precise prediction machines. They are structured ways of understanding relationships between risk and return under uncertainty.

Connecting Portfolio Theory and CAPM in Practice

In real investment decisions, portfolio theory and CAPM work together. Portfolio theory helps you understand how to construct efficient combinations of assets. CAPM helps you understand how those assets should be priced in equilibrium.

A practical investor does not evaluate stocks in isolation. Instead, they ask how each asset changes the overall risk of their portfolio. A stock that seems risky on its own might actually reduce risk when combined with other holdings due to diversification effects.

At the same time, CAPM provides a benchmark for expected return. If an asset offers more return than its beta justifies, it may be undervalued. If it offers less, it may be overpriced—at least in theory.

For example, a diversified investor holding a mix of technology, industrial, and consumer stocks may find that adding a low-beta utility stock reduces overall volatility more effectively than expected. Even if that utility stock seems “boring,” it plays an important role in shaping portfolio behavior.

FAQ

Key Terms Explained

- CAPM: A model that links expected return to systematic risk measured by beta.

- Beta: A measure of how sensitive an asset is to overall market movements.

- Efficient frontier: The set of optimal portfolios offering the best return for a given level of risk.

- Systematic risk: Market-wide risk that cannot be eliminated through diversification.

- Unsystematic risk: Asset-specific risk that can be reduced by holding a diversified portfolio.

- Capital Market Line: A line showing optimal combinations of risk-free and risky assets in portfolio construction.

The key shift in thinking is this: instead of asking “how risky is this stock?”, a better question is “how does this stock change the risk of everything I already own?” Try looking at your next investment decision through that lens rather than treating assets one by one.

References:

- https://www.youtube.com/watch?v=YkycWncVmUU

- https://www.youtube.com/watch?v=_RBevTla7pA

- https://www.youtube.com/watch?v=XIXd7pUt4cg

- https://www.investopedia.com/terms/c/capm.asp

- https://zoo.cs.yale.edu/classes/cs458/lectures/old2015/mpt/CAPM.html

- https://www.netsuite.com/portal/resource/articles/financial-management/capital-asset-pricing-model-capm.shtml

- https://frm.midhafin.com/part-1/modern-portfolio-theory-and-the-capital-asset-pricing-model

- https://www.remnote.com/learn/business/finance/portfolio-theory-asset-pricing-and-the-capm-study-deck

- https://hbr.org/1982/01/does-the-capital-asset-pricing-model-work

- https://gregorygundersen.com/blog/2022/03/06/capm/

- https://www.scribd.com/document/521477486/Portfolio-Theory-and-CAPM